Securing the Future: Cybersecurity’s Evolution & What’s On the Horizon

Introducing Sapphire Communities – A Robust Knowledge Network for Startup CEOs and Industry Leaders

A new platform to meet leading practitioners, discover best practices and uncover opportunities to drive business growth

With more than 170 portfolio company investments since the firm’s inception(¹), Sapphire is intimately familiar with the entrepreneurial journey and what it takes to build a category defining company. We know that oftentimes, it’s difficult for CEOs and company leaders to know where to go for guidance and how to get connected to leaders who have done it before. This, coupled with the current macro environment impacting the technology ecosystem, has resulted in startups requiring more help than ever to build their companies, and Sapphire is here to help.

At the same time, Global 2000 organizations and leading digitally cloud native companies are being tasked to innovate, create organizational efficiencies and meet the technology demands of today’s customers. We believe that startups are key to delivering on these evolving expectations, and Sapphire has been a crucial partner in providing access to the latest technology innovations and trends.

With this in mind, we’re excited to unveil Sapphire Communities. An extension of our value-add platform, Portfolio Growth, Sapphire Communities provide portfolio company executives, Global 2000 decision-makers and top private cloud company leaders with the opportunity to make connections, learn new strategies and accelerate business growth. Sapphire Communities is also made up of our in-house executives and Sapphire’s Growth Advisors. Also announced today, Sapphire Growth Advisors is an exclusive group of B2B technology leaders within our network who work closely with our companies to help them achieve their business goals.

Doing More With Less: Is Making the Move Upmarket Right For You?

“Do more with less.”

This mantra is echoing across the B2B technology startup landscape. After years of tremendous spending and growth, we believe 2023 will be the year that companies prioritize productivity over capacity.

While making this transition is easier said than done, focusing on generating more revenue per rep can be the hallmark of thriving and resilient companies.

Companies are thinking upmarket

Across our portfolio, we’ve seen a variety of approaches to optimizing productivity. One common theme is making the move upmarket.

It’s an enticing proposition, given the current economic climate. Technology companies are experiencing what Gartner calls the “triple squeeze”: continuing inflation; costly talent; and global supply challenges (caused by the war in Ukraine, COVID-19 and energy shortages). Despite this, large enterprises are still increasing IT budgets. This trend has been true historically, as larger companies tend to have stable budgets, come from a diverse set of verticals, and plan for a long time horizon, which means selling to the enterprise can lead to attractive net dollar retention.

Still, moving upmarket can be challenging. Unlocking an enterprise motion is a multi-year, “invest ahead” journey that forces you to rethink many facets of your go-to-market strategy, plan and execution. False starts are common.

As you consider making the move upmarket, the GTM advisors at Sapphire Ventures have come together to share a few thoughts on how to evaluate whether to make the move and how to get started.

While not comprehensive, our advice can serve as a helpful launch pad for the “upmarket curious.”

Should you go upmarket?

From our experience, there are three primary areas to evaluate in order to decide whether to go upmarket.

Push or pull: Start by asking yourself whether the move upmarket is organic and customer-led. Too often, companies convince themselves that they have an enterprise-ready product because they’ve closed a handful of enterprise deals. These deals don’t always reflect broader demand.

Take time to evaluate the market landscape and the whitespace available to you in the enterprise, given your product’s readiness for release. If you identify a clear and quantifiable opportunity, and you have multiple external data points pulling you upmarket, then you may have the right ingredients.

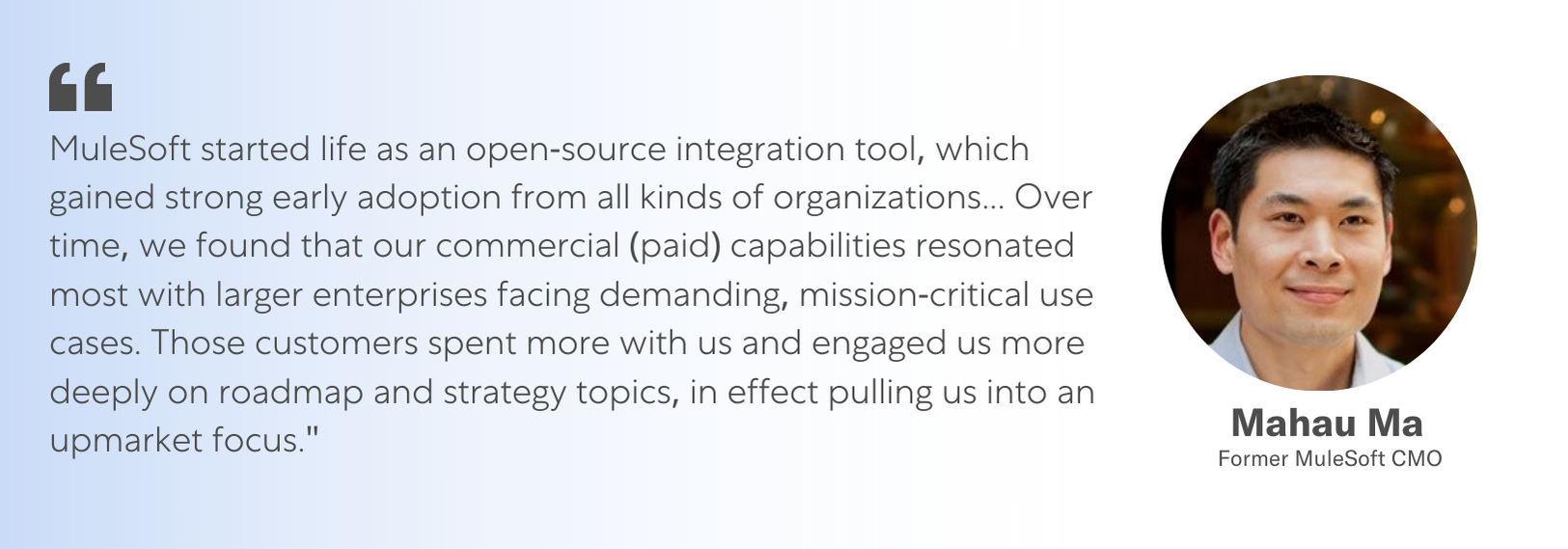

Our operating partner Mahau Ma, formerly CMO at MuleSoft(*), saw this in practice during his early days at the software company.

(*) denotes prior Sapphire Portfolio Company

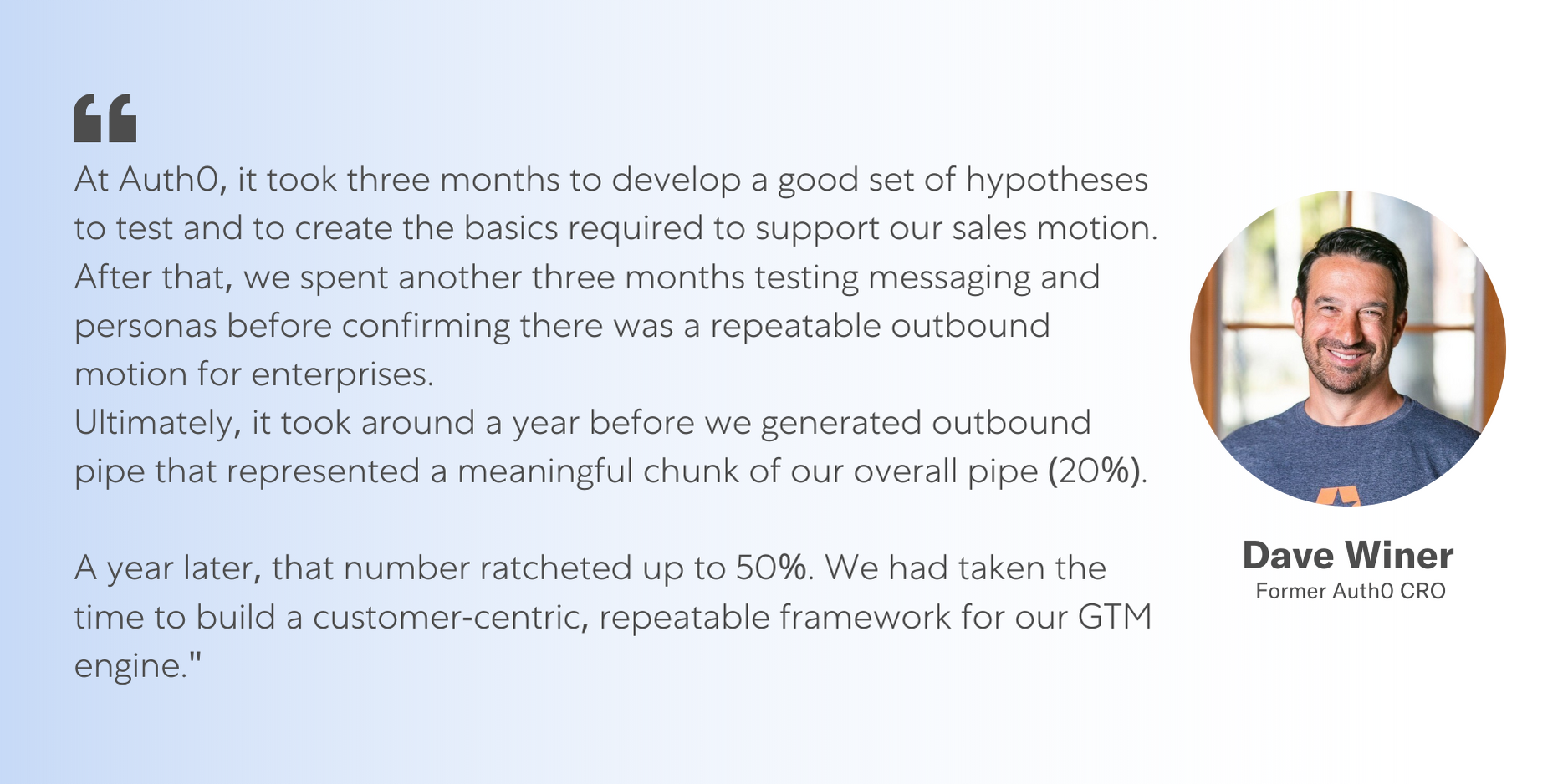

Validate and define: Once you have confidence in the market opportunity, go into testing and learning mode. Consider designating a small team (think one or two sellers, a product leader and a demand gen lead) who have air cover from their organization to focus on building out the basics of this segment.

The goal of this team is to determine the assets, process, technology and resourcing needed to effectively support a repeatable revenue motion. If you cannot define the entry criteria for moving upmarket, it will be difficult to invest resources into this pivot.

Dave Wilner, former CRO at Auth0, shares his experience in this journey:

Align the company: Making the move upmarket isn’t a sales strategy — it’s a company strategy. As you build the customer base upmarket, your product teams may need to develop enterprise-level functionality, marketing will need to tailor messaging and account-based strategies to support a different type of buyer, post-sales will need to offer more white-glove service and support and your G&A and Ops teams will need to develop tools and processes to help you navigate these sales cycles consistently. These expectations, and the associated resourcing needs, will only grow as you penetrate further into this market.

Take time to surface this strategic pivot at the company level. Try to align it against an OKR framework, so that the broader organization understands how it will be supporting this shift.

If you cannot build consensus across your leadership team, your foray upmarket is unlikely to succeed.

The block and tackling

Once you have made the decision to go upmarket, here’s what to prioritize in the early days:

Define the customer journey: You want your sellers to sell the way your buyers want to be sold to. To help facilitate this process, align your customers’ objectives and outcomes with the following stages:

What SaaS Profitability Looks Like in 2023

Coming off a tough 2022, we feel we are entering the “new normal” for SaaS valuation levels. While there’s been a lot of talk about how important profitability is in this new normal, we believe growth is still the most important metric. After all, we are using revenue multiples to value SaaS companies, not P/E multiples. This is because the best SaaS companies focus on acquiring customers and gaining share, executing against huge market opportunities – and then once at scale, they expect to be able to deliver meaningful profits to investors. We use revenue multiples as a proxy for a discounted cash flow analysis in SaaS because the majority of high-growth SaaS profits are 5+ years out.

Growth matters because higher top line often means more potential cash flows, but unit economics matter for the same reason: ultimately generating cash flows on the bottom line. This is why profitability is increasingly being discussed as the key second variable in the valuation equation. So let’s take a look at the levers of profitability and what a growing start-up should realistically assume, based on what we’ve seen over the past decade of investing in SaaS here at Sapphire Ventures.

Public Markets and Profitability

While “profitability” can mean different things to different investors, for SaaS companies, we tend to see focus on operating margin (EBIT). We believe operating margin paints a pretty good picture of a SaaS company’s ability to ultimately generate cash over the long term.

The first, and perhaps most important point to make, is that getting to profitability is difficult. Amongst the 56 comparable public companies that we use internally to benchmark our private companies, only 52% are expected to finish 2022 with positive EBIT margins. What stands out amongst this comp set? For one thing: size and growth. The median revenue of the EBIT positive companies is ~$1.3B, growing at ~28% YoY. In many ways, this is an obvious point. As companies scale, they gain more operating leverage across the entire business, enabling them to generate more profits.

The key to managing profitability, especially for a start-up, lies in how effectively and efficiently you can control the four key cost buckets listed below. (We plan to take a deeper look at some of these buckets in future blogs this year.)

- Cost of Goods Sold (COGS)

- Research & Development (R&D)

- Sales & Marketing (S&M)

- General & Administrative (G&A)

How do SaaS companies ultimately manage to profitability? Let’s take ServiceNow and Salesforce as examples of two mature software companies, still growing at scale (23% and 20% YoY growth for 2022, respectively). Both have gross margins of ~75%, which they were able to systematize as they scaled. Operating expenses as a % of revenue for both companies are in the 70-75% range, although how they get there looks slightly different. Both have G&A at around 10% of revenue, with strong consistency on this metric once they reached scale. At the margin, Salesforce spends more on S&M (~45% of revenue, which is a sticking point with Wall Street analysts by the way), while ServiceNow spends relatively more on R&D (~23% of revenue).

Both ServiceNow and Salesforce demonstrate what profitability at scale looks like: positive EBIT margins, driven by consistent growth, controlled G&A spend and investments in key business drivers (S&M for Salesforce, R&D for ServiceNow) – all leading to 20%+ cash flow margins.

Key Takeaways for Ambitious Start-Ups

The companies in our public comp set can serve as inspirations for the future, not benchmarks for where your SaaS company should be today. That being said, it’s never too early to start thinking about what your company might look like at scale. And with increased investor interest in managing to profitability more quickly, understanding bottom-line levers and the steady state of your business is more important than ever.

We have access to many of these public SaaS companies’ financials when they were private companies, both via public filings and due to our diligence on the companies when they were private. The trendlines from this data are clear (charted below): S&M spend accounts for the largest portion of operating expenses, but also decreases the most on an absolute percentage basis over time. This suggests that market tailwinds and product-market fit are critical to maintaining growth when you decide to pull the S&M lever to push toward profitability.

The 2023 European CIO Outlook: 4 Pressing Challenges Impacting Enterprises

Whether it’s economic turmoil driving enterprises to explore new avenues for innovation or whether we’re seeing a new era of low-barrier, rapid innovation, one thing is clear. Heading into 2023, the responsibilities of the European CIO are larger than ever–and, some might say, overflowing.

From security, sustainability, governance and digital transformation to data, AI and Web3, the set of challenges is ever-growing for today’s CIOs.

We heard firsthand about the growing demands being placed on today’s CIOs at the 2022 Sapphire Vision Summit, Europe. While our past summits focused on macro themes such as the pandemic and its aftermath, emerging technology trends amidst a rise in ESG priorities, the metaverse and more, this year’s event focused on a range of CIO-related topics.

From what we heard at the summit and throughout the past several months in dozens of conversations with our network, we see four pressing challenges impacting the European CIO heading into 2023:

- The ballooning responsibilities of CIOs and IT leaders

- The gap between enterprise buyers and startup sellers is slowing innovation

- The complex path to financially viable AI

- The convergence of sustainability and wider company strategy

Let’s take a closer look at each.

The responsibilities of today’s CIO are ballooning

From AI to sustainability to security to Web3, leaders are now expected to maintain a panoramic view over a vast number of technological developments outside of the organization.

With new tech emerging seemingly every moment, the demand for new tools is also seeping into the organization, with 76% of global CIOs and CTOs citing an increase in demand for new digital products and services.

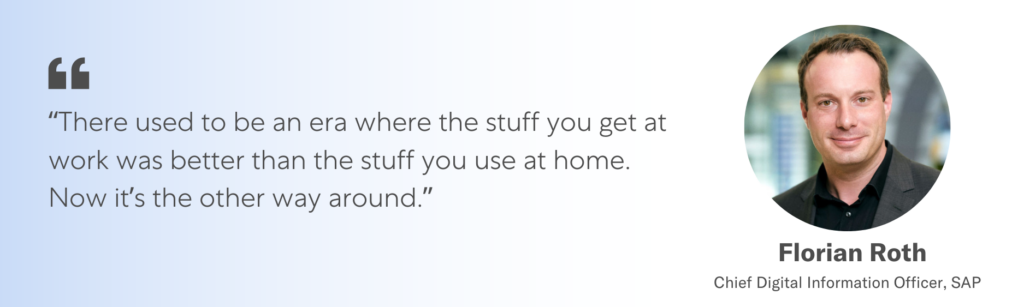

But as Florian Roth, Chief Digital Information Officer at SAP explained at our Vision Summit last year, this isn’t just a shift in the demand for new digital tools, a complete shift in employee expectations continues to be a challenge for enterprises. “There used to be an era where the stuff you get at work was better than the stuff you use at home. Now it’s the other way around.” The consumerization of IT is nothing new, but now we’re seeing employees demand the ease of use, innovation and convenience of personal apps and tech experiences in their work platforms. Oftentimes, it’s startups that are able to deliver on these new employee expectations.

This tech trickle-down effect is asking CIOs to rethink the way they balance the scales of control and innovation. As Patrick Naef, Partner at Boyden and a speaker at the 2022 Sapphire Vision Summit, Europe, outlines in his ebook, The future of IT, “While cost might have been optimized by centralizing all of IT, the downside was that speed and innovation suffered from such an approach.”

In response to growing responsibilities, CIOs are adjusting their focus to be more agile. But how are they planning to do that? As Florian explains, it’s about accepting less control. “I want to have control of the most important products, but on the other side, we need to agree there is certain flexibility and freedom for choice of tooling – especially in the engineering space.“

As CIOs take a more active role in enabling new tech and innovation within their organizations, they must also look externally for help. As Naef puts it, “A modern CIO needs to be more entrepreneurial and less operational, meaning less risk- or cost-focussed.”

Startup engagement needs to meet in the middle

Another trend, this time from startup founders, revolves around their engagement experiences with the enterprise. Specifically, it is very difficult to work with large organizations.

In a discussion led by Sifted’s Head of Intelligence Chris Sisserian at our 2022 Sapphire Vision Summit, Europe, we heard that despite enterprises pursuing smaller businesses as a means of innovation and flexibility, startups were finding it difficult to work with these customers due to inefficient procurement cycles and difficult deal terms. Some startups end up prioritizing non-Enterprise sales opportunities because the cycles are faster and have less customization.

One of the biggest hurdles for startups is that enterprises haven’t adapted their legal requirements. Many startups find an 18- to 24-month enterprise sales cycle too high in cost and risk. Couple slow engagements with only 15% of enterprise IT spend allocated to startups and it’s clear the path for startups to work with enterprises could be made much easier.

Chris from Sifted offers a solution for innovation-hungry enterprises, “…finding a way to build a ‘start-up’ focused team internally can build a better rapport and speed up the process.”

However, this isn’t a one-sided struggle. Enterprises offer more stability in the uncertain economic times we face today. That means startups must meet enterprises in the middle, by improving their flexibility and adapting their buying cycle to fit in larger PoCs and maximize value.

Beyond the basics, for a startup to engage with an enterprise, CIOs at these large European companies like to understand how they will save on cost and see greater efficiencies. Most of the time, this is far more important than getting caught in the technical weeds.

As efficient innovation becomes a bigger focus in 2023 for CIOs and economic uncertainty has startups looking for more secure customers, a meeting in the middle is on the horizon.

A long and winding road to effective AI adoption

The AI conversation for CIOs and enterprises globally has moved beyond ‘should I invest in AI?’’ to ‘what kind of AI do I need?’

At the most collaborative end of the spectrum, AI can act as an “illuminator” that generates inputs for co-creation with humans. For example, Ben and Jerry’s used AI to process unstructured data in popular media to discover a demand for “breakfast ice cream.”

On the other end, there’s automated AI that can decide and implement decisions with human oversight, such as Rio Tinto’s autonomous mining that uses advanced robotics and AI technology to simultaneously manage loaders, haul trucks and rock crushers, making sure equipment is in the right place at the right time.

The promise of AI innovation is tantalizing, but there’s a widening gap between the idea of AI and its application–only 10% of companies today report significant financial benefits from AI.

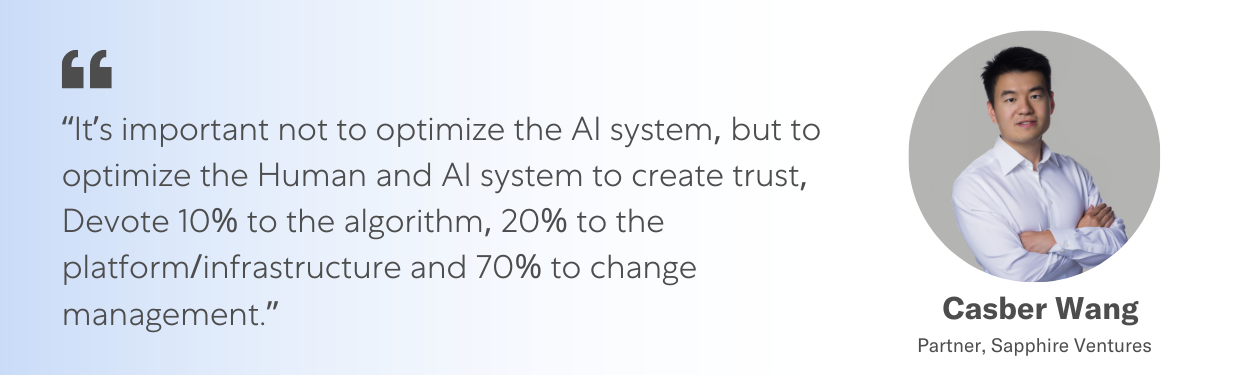

So how can European CIOs roll out profitable AI for the enterprise? Francois Candelon, Head of the BCG Henderson Institute and leader of their Enterprise AI practice, hammered home the important interplay between AI and humans in successful AI adoption at our recent Summit. “It’s important not to optimize the AI system, but to optimize the Human and AI system to create trust, Devote 10% to the algorithm, 20% to the platform/infrastructure and 70% to change management.“

Francois’ research also lays out a four-phase approach to implementing profitable AI in the enterprise.

He suggests enterprises start with an initial discovery phase where enterprises implement specific AI applications, infrastructure and strategy. This might look something like implementing a sales model that reduces customer churn by 2%. From there, it’s about building AI applications for more specific business cases and investing in data, technology and algorithms to build AI capabilities across the organization.

With the right capabilities in place, enterprises are then ready to scale AI. With a growing number of technology options, effectively scaling AI becomes a matter of matching the right technology to a specific problem. Our very own Partner Casber Wang expertly outlines evolving AI tooling and how it’s trending towards more modular solutions for specific enterprise uses in a recent piece. This scaling stage also encourages a change from AI teams who solve specific problems to cross-functional teams that lend AI expertise across enterprise challenges.

Finally, for AI to be truly effective in the organization, Francois says enterprises must reach a level of organizational learning and adaptation so that trust in the tools can be nurtured. Getting this right has shown a 75% chance of positive financial impact for companies.

Sustainability and strategy are converging

Sustainable IT is a fast-rising conversation, especially amongst European CIOs who must contend with more stringent government regulations than their US counterparts. Consumers expect sustainability from brands and many are now making choices based on sustainability beliefs. In turn, companies are making changes to meet customers’ sustainability expectations. And that change is fast underway as more than 1/3 of Europe’s largest public companies now have a net-zero plan in place and CIOs are on the frontline of the push, with 65% adjusting their technology strategies to include the adoption of sustainability tools.

For enterprise leaders, that means viewing energy consumption, software, business practices and supply chains the same way you view all other emissions. Or as Annalise Dragic put it at the 2022 Sapphire Vision Summit, Europe, “Regardless of what you deem scope 1, 2 or 3 emissions, we’re all connected as an ecosystem that we need to propel forward.“

Though the major driver of this increased emphasis on sustainability is from outside influences such as customers, shareholders and other businesses, what we’re hearing from enterprise leaders is that addressing outside influences starts by getting buy-in from employees.

This means getting your net-zero story right internally, then going external with your goals–rather than letting external pressures influence how your company assesses sustainability. A large part of getting aligned internally comes from accountability through visibility, something in which CIOs already have significant experience from previous technology pushes.

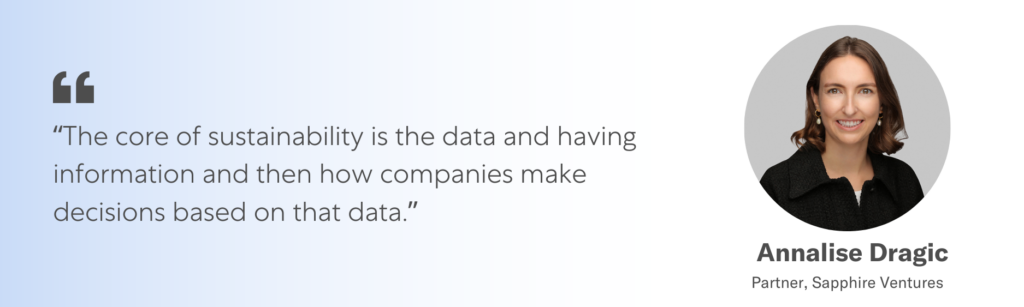

On one end, CIOs must be connected to the technology that’s bringing visibility to sustainability efforts. As Sapphire Partner Annalise Dragic put it, “The core of sustainability is the data and having information and then how companies make decisions based on that data.”

Additional big ideas

Cloud migrations continue to evolve in complexity

Cloud migration, a transformation all enterprises are in the throes of, continues to be a staged approach that needs to be continually assessed from a financial and functional perspective. And as the adoption of new data-hungry technologies like AI ramp up, the complexity of controls and compliance will only face great scrutiny.

Cybersecurity faces more attack surfaces than ever

With more digital transformation–new tools, data and the rise of multi-cloud–the digital attack surface of enterprises is larger than ever. To combat rising threats, enterprises need to engage in stronger defense practices, such as deploying purple team and tabletop exercises and adopting zero-trust standards with strong user-access protocols, protected backups and a segmented network.

The importance of being Web3-ready

Web3 is set to change the way companies and consumers interact. A shift from company-owned data to user-owned data will require a paradigm shift in value creation for companies. Leading the way in this transformation are luxury brands like Gucci, that have NFT art exhibitions tied to their heritage. While enterprises will need to tread carefully in the wake of FTX, there is still a tremendous amount of opportunity ahead for broader blockchain innovations.

Adaptability is key

As 2023 unfolds, there will undoubtedly be new moments and technologies that will shift European CIO priorities. While we don’t exactly know what those changes will look like, we know that today’s CIO must be flexible and adapt.

We will continue to share updates and trends from European and global CIOs throughout the year, but for now, you can dig deeper into the insights in this piece by watching the sessions from the recent 2022 Sapphire Vision Summit, Europe.

AI: Paving the Future of Digital Healthcare

It’s undeniable that one of the hottest topics right now is AI. While recently much of the buzz has centered around generative AI use-cases, we think that long-term, one of the areas where AI will have the greatest impact is healthcare.

While the adoption of AI solutions for healthcare has historically been slow due to long sales cycles, siloed data and regulatory considerations, we are seeing signs that this is beginning to change and are excited about what the future holds.

The Future of AI in Healthcare

When it comes to AI and healthcare, early applications have been for drug discovery and diagnostics. Biotech companies received $34B in venture funding in 2021 (more than double 2020). Not only has investment boomed in biotech, but we’ve seen some notable public outcomes such as Recursion, Exscientia and 23andMe (a Sapphire portfolio company) pushing the envelope on how drugs are discovered, developed and tested. There has also been a lot of excitement on the diagnostic side. Radiology, in particular, has been one of the earliest adopters of AI technology. Companies like Aidoc and Viz.ai have enabled radiologists to work more efficiently and effectively by detecting dangerous conditions and allowing radiologists to read scans more quickly.

Drug development and radiology are just the tip of the iceberg for AI/ML in healthcare. We believe we’re on the precipice of a wave of innovation driven by AI/ML for providers across three key workflows: data and analytics, clinical interactions, and administrative workflows. Our conviction comes from broader work we are doing to understand the key technologies and trends pushing healthcare forward, which we explored in greater detail in an earlier blog post.

Below we outline the series of events that have unfolded, which has created the perfect time for the increasing adoption of AI/ML technologies. From there, we’ll dive into a few categories and use cases where we are seeing companies build useful products.

Strike While the Iron is Hot: 5 Trends That Enable AI/ML in Healthcare

In meeting with many AI/ML and healthcare startups, as well as enterprises in our network to better understand where opportunities for innovation exist and where the healthcare industry can benefit, five key trends have emerged as to why AI/ML may start to play a more meaningful role in healthcare going forward.

COVID challenges opened new doors for innovation

COVID proved that healthcare can be delivered virtually, and be equally as effective as in person care in many instances. Medicare visits conducted by telehealth were 63x higher in 2020 than they were in 2019, resulting in 64% of providers being more comfortable using telehealth. Furthermore, 21 states changed their laws entirely to make telehealth access and payment reimbursement more equitable.

The increased adoption of digital healthcare technologies during the pandemic has changed how medical professionals perceive technology within their field. Forced to adapt, doctors quickly changed their processes on the fly, while still delivering better patient care. As we’ve written about before, the pandemic has accelerated the adoption of digital technologies within healthcare in a way that is equivalent to years of traditional GTM sales and market education.

This new found popularity in telehealth is a big win for the future of AI/ML in the space. Case in point: 2021 was a peak year of health tech funding. Even though investment activity declined in 2022, we believe more investors are now spending time in the space, which means there will likely be more dollars available for innovative AI/ML companies.

Doing more with less: how tech addresses the labor shortage

Despite the layoffs in tech, the broader US economy continues to face a labor shortage. One area where this shortage is particularly acute is healthcare. Driven to burnout by the extraordinary pressures faced during the pandemic, nurses have quit their jobs in droves (one account suggests that ~20% of nurses quit their job during the pandemic). This leaves many hospitals understaffed, with some estimates of the nursing vacancy rate as high as 30%.

Much of this trend is driven by the amount of time spent on non-patient interactions. Nurses spend up to 25% of their time on documentation. Doctors, too, are constantly seeking ways to do more with less. A study found that 30% of doctors spend more than 20 hours a week on administrative tasks.

And in an environment where the supply and demand imbalance is only expected to increase as the population ages, healthcare workers will have to become more efficient than ever. AI promises to drive automation and increase efficiency through better care management and reductions in administrative burdens.

Efficiencies from Digital Healthcare Helping Curb Operational Costs

Another major challenge facing the healthcare industry is increasing costs–across both providers and patients. Data continues to show that Americans struggle to afford healthcare, while providers are operating with negative margins.

Medical costs have far outpaced overall inflation–the CPI for medical care is up, on average, 3.5% per year over the last 20 years, while the overall CPI has grown, on average, 2.1% per year. Despite this, providers are still struggling to operate profitably, as it is becoming increasingly expensive to treat patients over longer stays, in part due to sicker patients and increased prices for medical supplies.

While technology is not a cure-all for lowering expenses (particularly since some portion of cost increases are due to increased adoption of high-priced technologies), we do believe that improved outcomes and operational efficiencies driven by new technologies in digital healthcare will play a role in slowing the rise of healthcare costs.

Practitioners are increasingly comfortable with AI-powered tools

As we’ve spoken with doctors and other clinicians over the past few months, we’ve heard a recurring sentiment, “Our peers in other industries are leveraging AI-based technologies successfully–how can we use these tools, as well?”

Data supports this anecdote. Optum recently found that 74% of healthcare leaders now trust AI to support non-clinical workflows. While patient trust in AI-driven diagnoses remains mixed, the upside of non-clinical use cases is that the decision ultimately lies with the practitioner and doesn’t directly impact clinical diagnoses.

Given that the stakes are in most cases higher in healthcare than say, enterprise SaaS, it’s understandable that doctors are cautious when it comes to the adoption of new technology. But as AI/ML use cases continue to take hold in the everyday lives of healthcare practitioners, we anticipate more willingness to adopt AI-based solutions, particularly for non-clinical use cases.

The introduction of LLMs and continued investment in basic research

OpenAI released the next iteration of its powerful Generative Pre-trained Transformer model (GPT-3), with rumors of the next version (GPT-4) being released later this year. Trained on hundreds of billions of words across a variety of data sources, GPT-3 represents one of the most advanced large language models (LLM) built to-date.

In the same vein, researchers at Google/DeepMind recently fine-tuned Flan-PaLM to a medical-specific context. The resulting model, Med-PaLM performed close to physician-level on answering long-form medical questions.

Much of this explosion in LLMs has been driven by basic research. The number of AI patents filed in 2021 was 30x higher than the number filed in 2015. This research, funded by universities, governments and private companies, will continue to drive innovation and provide the basic building blocks with which startups can create the next generation of companies.

Three Areas of AI/ML Opportunity for Providers

Sapphire Roundtable Recap: How Startups Plan to Tackle Revenue Growth in 2023

New year, different environment, same drive and ambition for our portfolio companies to build an enduring business.

Kicking off 2023, our goal here at Sapphire is to provide revenue leaders across our portfolio with best practices in approaching growth during a time when companies are being asked to do more with less. That’s why we recently held a roundtable discussion on the topic.

In thinking about the recent conversation, a number of interesting insights surfaced that we felt made sense to share more broadly. Here they are:

- Selling to buyers is becoming more challenging as companies grapple with buying indecision. Sellers need to counter-steer the process by being adaptive in the current selling environment. Rather than going all or nothing on the full deal, consider selling a smaller portion of the deal this year and then upselling the rest of the deal in the following years.

- Many top sellers are also shifting from selling what they think customers want to providing recommendations on what customers “should” buy. Instead of paraphrasing an already excellent read on the topic, check out this HBR article on the important topic of buyer indecision and the steps you can take to help your sellers overcome it. These course corrections techniques require additional training for your sales team to operate in a different environment.

- Avoid leaning on maximizing discounts to win deals. Many companies are giving too many discounts upfront to drive deal conversion. Instead, minimize your first deal discount and focus on driving value via success teams and prepare for a larger follow-on. Otherwise, you risk setting precedence for all future deals. During our session, we role-played with WBD selling a deal using this framework on how to trade instead of negotiate

- 2023 is about tuning your team to drive market share. Now may be the time to focus on new logo acquisition to maintain a robust customer base and position the team for expansion sales. Many companies will see higher churn and account contractions unfamiliar in recent years, especially to revenue practitioners who have only experienced the tech boom of the last decade. The focus on new logo acquisition in 2023 is about building a pipeline of accounts that will help mitigate declines in net dollar retention. To help make this transition:

- Senior sales executives will need to develop and train junior sales and customer success teams to handle customers asking for early contract churn. A lot of this is centered around messaging and objection-handling resources that we can offer our sales and success teams.

- Leaders will need to focus on ‘training the trainers’ – i.e. providing support to their front-line and second-line managers. Too often, successful sales reps or CSMs are promoted into management positions but are not given the proper training to succeed in their new role. For revenue managers to have an impact, they need to learn how to keep tabs on metrics and more importantly, how to become true coaches to their teams. When done right, it’s a multiplier for the organization.

- Many companies are shifting their focus to Enterprise sales. While it can be a lucrative GTM shift, this requires an entirely new GTM motion and a new mindset for the company. To support the build-out of an enterprise GTM motion, revenue teams will have numerous internal considerations to get right:

- Limit the number of GTM motions. Too many GTM motions prevent teams from optimizing. Each motion requires marketing, customers, sales teams, finance, and HR resources and time. For companies with sub-$50 million ARR, 2-3 GTM motions is the maximum number recommended.

- Align compensation and incentive structure to enterprise deal generation and development. Work with your compensation teams (typically a mixture of total rewards, finance, and revenue planning groups) to set up the right incentives for your revenue teams. Leverage external benchmarking data for OTE guidelines and be open to structuring a multi-year compensation plan when first diving into Enterprise.

- Tiering your sales team within each sales bracket. To help build a career path for your Enterprise team which allows both external hires and internal promotions, you will want to consider having a three-point system. By having Junior, Mid and Senior AE roles within Enterprise, you can have a blend of internal and external talent brought in without breaking your budget. Just be mindful that quota needs to connect with OTEs, so your lower tier reps will have lower quotas than your senior reps.

We always enjoy bringing together Sapphire portfolio leaders and guests to our GTM events, and this kick-off roundtable is no different. With 2023 well underway, now’s the time to start acting on some of these insights and best practices for practitioners.

If you have additional questions about our upcoming GTM events or want to dig deeper following this read, you can reach me at [email protected].

SaaS Stocks: In It to Win It, Why We Remain Long-Term Bullish on Next-Gen SaaS

Let’s cut right to the chase – 2022 was a challenging year for SaaS stocks. On November 9, 2021, the Nasdaq Emerging Cloud Index (which tracks a cohort of 76 cloud companies) hit an all-time high. On that same date, Sapphire’s internal index of public SaaS companies also hit a high-water mark.

But since then, it’s been all downhill. The Emerging Cloud Index finished 2022 down ~52%, while the Sapphire broad SaaS index was down ~55%. The tech-heavy Nasdaq finished the year deep into bear market territory, down ~33%1.

Will Current Market Conditions Cause Unicorn Status to Lose its Lustre?

An abridged version of this article by Annalise Dragic was originally placed in City A.M. on December 16, 2022 under the headline “Unicorn status is no longer the holy grail of success for start ups in the UK and Europe.”

After several record breaking years for the European startup ecosystem, 2022 marked a new, more volatile environment. The pace and focus of venture investments has shifted as the market faces a notably altered economic climate. While brilliant businesses are continuing to raise strong funding rounds, this has been happening against a backdrop of postponed IPOs and decreasing valuations in the space.

As we navigate this new landscape and valuations continue to fall (the most headline grabbing so far include Klarna, which has seen a 85% drop in its valuation compared to this time last year), we are confronted by the question of how we should rethink our evaluation of startup success. Should we still put so much weight behind “unicorn status” when measured against the current macroeconomic picture? Or should we instead be looking at Annual Recurring Revenue (ARR) or other cash flow metrics?

Since the term was first coined in 2013, unicorn status (defined as reaching a $1bn valuation) has become a pinnacle of startup success. It’s the way regions compare the maturity of their tech ecosystems and a metaphor the media has embraced. There are currently 189 privately held unicorns in Europe, many produced in 2021 when record levels of venture investment were flowing into the European innovation scene, bigger deals were being closed, and more companies went public.

I believe this growing crowd marked distinct individual and collective success; offering clear confirmation that the European tech market is continuing to rapidly mature. However, the lustre of the unicorn status may be fading.

It seems to be that this can be attributed to two main, and potentially conflicting, drivers. Firstly, the last few years saw such a rush of capital being poured into European markets that the unicorn herd quickly became a stampede. This pace meant that we became accustomed to companies raising VC rounds in quick succession and hitting unicorn status within a few years of being founded. A case in point was virtual events platform Hopin’s sprint from launch in October 2019 to a £1.37bn valuation in November 2020.

This sparked what some might describe as unicorn complacency. No longer such a rare beast, buzzy startups were almost expected to reach billion dollar heights at a rapid pace. Perhaps predictably, attention during the 2021 European tech boom turned to decacorns – those with a $10bn valuation – as the new marker of real success.

It feels like the ‘mainstreaming’ of unicorn status did the title a disservice. Reaching a $1bn valuation is an incredible achievement that only a small sliver of startups are ever able to reach. Despite the outsized attention that this small fraction of start-ups received in recent years, they remain an elite club.

The second dent in unicorn prestige was made at the beginning of the current tech market cool down. Against the backdrop of new economic realities, valuations are being recalibrated accordingly. VCs and start-ups alike are watching market forces closely as these numbers settle. Some of those who once held unicorn status are starting to fall out of the club.

This combination of intense acceleration in unicorn numbers, followed by the sharp market correction we’re currently experiencing, has led some to champion other mythical beasts as the new market of ‘true’ start-up success, like the ‘centaur’. Proponents of this label – which is bestowed upon a business when it hits $100m in ARR – argue it’s a more accurate measure of success at a time when cash is king and valuations are a moving target. And technology companies which are generating significant revenue may be in a much stronger position going into what looks likely to be a global recession.

As a European tech community, we can and should do more to celebrate those companies that reach $100M ARR and those that – gasp – also build profitability from day one to reach a significant scale. That said, we should continue to celebrate our unicorns. Building a company from scratch and scaling it to a valuation of $1 Billion should not be downplayed nor overlooked. And the fact that more companies have continued to join the European stable in 2022 despite the macroeconomic climate is testament to the region’s strength. And the current landscape of shifting valuations may mean unicorn status carries even more weight as businesses continue to scale while facing macroeconomic challenges.

Now may be the time to add more nuance to our tech success benchmarks, but we don’t need to sweep away existing ones in the process. Instead, we should be broadening the stable – bringing centaurs into the herd, along with unicorns, and embracing other milestones too. From my experience, the majority of VCs and founders continue to take unicorn status seriously and it would be a mistake to dismiss this valuable term, even as we seek new ways of categorising achievement and growth.

While we embrace more mythical creatures as markers of success, I believe the era of the unicorn is far from over.