Navigating a New Normal: GTM Learnings From Our Inaugural Sapphire Ascend Summit

Germany’s Booming Startup Scene, in Berlin and Beyond…

Germany’s startup ecosystem has grown remarkably over the last two decades, helped by a supportive regulatory environment, access to capital and an academic structure and culture that encourage entrepreneurialism. The country has produced 30+ unicorns and, according to Sifted and the German Startup Monitor 2022, is home to over 20,000 startups employing more than 620,000 people across fintech, cybersecurity, cleantech, climate tech, enterprise software and many other sectors. We have been taking a look at the trends to understand the drivers behind Germany’s next wave of innovators.

Funding the Future

Building on a rich history of industrial innovation, Germany’s startup landscape has attracted entrepreneurs, investors and talent from around the world. It looks like entrepreneurship is likely to continue thriving, with the German Startup Association recording a 16% increase in the number of startups in the first half of 2023. German startups have benefited from a strong funding environment to support the ambitions of founders, with ~$72B in total funding over the last decade and the importance of startups to the wider economy is well-recognised in Germany. For example, the German government established the High-Tech Gründerfonds (HTGF) to provide early-stage financing and support to innovative startups. Its portfolio includes SimScale, a 3D engineering simulation platform, and Natif AI, an intelligent document processing and automation platform. Dozens of other local and national organisations, supported by private and public investors, have played a crucial role in providing capital, mentorship and networking opportunities to fuel the success of German startups.

Time to Hit the Autobahn

We believe it is clear that the German startup landscape is becoming ever more federated, with hubs of research and innovation flourishing across the country. In Sifted’s 2023 Rising 100 list of B2B SaaS startups in Europe and Israel, 19 of the companies were based in six cities across Germany. As further evidence, StartupBlink’s Global Startup Ecosystem Index included 40 German cities in the 2023 ranking. In this piece, we will take a closer look at 3 of the biggest tech hotspots: Berlin, Munich and Cologne.

Celebrating What’s New and Next

At Sapphire Partners, we have long believed in the importance of emerging managers in the venture capital ecosystem and more specifically as an integral part of an LP’s portfolio. When we launched our LP investing work a decade ago, we intentionally built a strategy that included investing in emerging managers as a component of our early stage venture fund portfolio. To date 80%(1) of all the US emerging managers venture funds we have invested in (defined as Vintages I – III) have since gone on to raise subsequent funds such that they are now considered established managers (which we define as any vintage IV+).

Today I am delighted to announce Sapphire Partners is launching a new emerging managers investment program with a sole LP, CalSTRS, the world’s largest educator-only pension fund with 1 million(+) members and beneficiaries. For decades CalSTRS has held a similar conviction in the power and promise of emerging early stage venture managers, making them a natural partner for us.

As a part of this program, Sapphire Partners will take over the management of five existing CalSTRS “New and Next Generation Manager Funds”, representing $1.4 billion AUM(2). Together, we will have collectively partnered with more than 300 emerging manager-led funds. And going forward, we plan to deploy approximately $100M/year into emerging venture managers. This new program complements our existing LP work of investing in early stage VCs in the US, Europe and Israel. (You can read more about the announcement here.)

Emerging managers are a critical part of the VC ecosystem

As much as today is about celebrating our new partnership with CalSTRS, our dual focus is on the emerging manager. It is important to remember that venture funds, even the legendary ones like Accel, Benchmark, Sequoia, Union Square, etc., all were first time funds once upon a time. Like all the emerging managers that have come since, they brought new ways of thinking, investing, grit and the hustle to attract the next great entrepreneur. And while being an emerging manager in no way guarantees your financial success, funds led by emerging managers made up 72% of the top returning VC firms between 2004 and 2016, according to Cambridge Associates(3).

Streaming Wars: Video Security & Video Intelligence Edition

The Video Security market is at an inflection point. Technological advances have replaced legacy approaches with modern security systems that integrate hardware and software or equip existing cameras with modern cloud and computer vision capabilities. After getting off the ground in the last 5-10 years, next-generation players have started to gain meaningful traction in the market, which boasts a market size of at least $10B within the US alone.

Simultaneously, the nascent category of Video Intelligence is starting to emerge. Video Intelligence builds on the success of using video data for physical security and public safety by developing tailor-made software and insights for other use cases, such as workforce management, customer experience, store performance, sports analytics, etc. As the Video Intelligence category matures, every professional will eventually be able to access insights and analytics from video data to support day-to-day objectives.

In this post, we break down how the Video Security and Video Intelligence categories have evolved to date, where both are headed next and what it will take for vendors to build dominant businesses in each category.

Video Security’s Netflix Moment

Prior to 2010, video security systems consisted of cameras connected to an on-premises recording and storage device, such as a digital video recorder (DVR) or network video recorder (NVR). We refer to this as Phase 1 of video security system architecture.

Introducing Sapphire’s ESG Framework & Inaugural Report

In response to heightened awareness of global challenges such as climate change, social equality and the long-term sustainability of business practices, investors and operators have increasingly focused on the importance of sustainability and diversity. As a result, Environmental, Social & Governance (ESG) frameworks have risen in prominence as a solution for guiding businesses towards responsible practices and enabling them to consider the impacts of their operations. As of 2020, nearly 90% of publicly traded companies, 79% of venture and private equity-backed companies, and 67% of privately-owned companies had ESG initiatives in place.

As more and more publicly traded companies adopt and report on ESG strategies, as soon to be required by U.S. federal regulators, private companies, especially those at the later stage nearing public debuts, are also beginning to adopt ESG frameworks to set themselves up for future success. At Sapphire, we aim to back Companies of Consequence, which we define as enduring businesses that have the potential to become category leaders. The way we see it, an enduring business should also actively account for ESG in its operations and continuously strive for improvement.

As an active participant in the VC and startup ecosystem, we understand the importance of building a more sustainable and diverse environment–both within our firm and at the companies we back. While we hadn’t yet formalized our approach or developed an official framework, our ESG journey started several years ago when we began to incorporate a term sheet rider committing our portfolio companies to diverse recruiting efforts, tracking our internal employee diversity and inclusion and partnering with organizations such as Black Women on Boards, AllRaise, The Mom Project and Screendoor to advance diversity across the VC and startup ecosystem. We also began our sustainability journey by tracking our carbon footprint, incorporating sustainable office practices and purchasing high quality carbon removals from Charm Industrial.

Over the past year, we furthered our ESG efforts by building a comprehensive program targeted at integrating ESG across all facets of our business, including the sustainability of our internal operations, investment sourcing and decision-making, portfolio company governance, monitoring and advisory support, and our local community impact. As a first step in this process, we felt we had to understand where we and our portfolio stood on key ESG metrics. To do this, we developed an ESG framework that we believed incorporated our values at Sapphire and would be most impactful for the companies (size, stage, sector, etc.) in which we invest. It took us some time to gather all of the relevant internal and portfolio-level data and then translate the findings into meaningful results, but after months in development, we are now publicly sharing our Sapphire ESG Framework and inaugural 2022 ESG Report.

In building our report, we focused on five core ESG pillars that we believe are most impactful for our stakeholders: environmental sustainability, executive and board director diversity, inclusive and equitable workplaces, board and LPAC governance, and data privacy and security. Here is a brief summary of our findings:

- Environmental Sustainability: Earlier this year, we joined the Venture Climate Alliance, which commits us to achieving operational net zero by 2030 and encouraging our portfolio companies to achieve net zero by 2050. In an effort to reduce our carbon footprint, last year we conducted our second carbon audit and incorporated new strategies into our operations to reduce it. Although we have not yet achieved net zero, we have made progress by purchasing carbon offsets from Charm Industrial and Pachama to cover our entire carbon footprint for 2022.[1]

- Executive and Board Director Diversity: For the first time ever, we have published our internal employee level diversity data, portfolio company board level diversity, the diversity of our portfolio CEOs, the diversity of our GPs and the diversity of our investment pipeline. The findings show that there continues to be room for improvement, and we will continue to actively work on measures to address.

- Equitable and Inclusive Workplaces: We believe that equitable and inclusive workplaces where all employees are treated fairly and have the resources they need to effectively contribute are essential for building a sustainable and effective organization. To achieve this, we assess our employee engagement and the equality and inclusivity of our workplace annually, which is disclosed in our report. Additionally, we have expanded our equity program to include more than 70% of our workforce, including many of our non-investment professionals, and at our portfolio companies, 84% of their employees share in equity compensation.

- Board/LPAC Governance: Boards and LPACs are essential corporate structures enabling effective decision-making at the portfolio company and portfolio fund level, respectively. We generally seek board and LPAC representation in our investments and help our companies place independent board directors that are critical for finding balance between investors and founders.

- Data Security and Privacy: Data security and privacy are crucial for ensuring the privilege to serve customers, protecting key stakeholder data and complying with regulation. As part of these efforts, we track company data security policies, as well as critical data breaches.

While regularly reporting on these areas is critical to understanding progress and priorities, we find it equally as important to help support our portfolio companies on their ESG activities. As they embark on their growth journeys, many are starting to think through best ways to implement ESG practices, and we are here to help. Earlier this year, we introduced Sapphire Communities where our team provides portfolio company CEOs and leaders with access to our networks, knowledge centers and exclusive events. Sapphire Communities include: Finance, Engineering, People, IT, Revenue and ESG. The purpose of our ESG Community is to provide our portfolio companies with the tools and resources they need to accelerate their ESG maturity and to help Sapphire continue to evolve our ESG framework. If you are a practitioner interested in joining Sapphire’s ESG Community, please reach out to Sam Procter at [email protected].

We believe incorporating ESG considerations into operations will become table stakes for founders and executives seeking to build Companies of Consequence. We hope that by gathering and sharing our ESG framework and report with the broader ecosystem, we can improve transparency, help our community and stakeholders productively engage on ESG matters, and continue to advance learnings and best practices on these topics. To this end, please don’t hesitate to reach out with any questions or comments – we’d love to hear from you.

How to Adopt Consumption-Based Pricing — and Avoid Common Pitfalls

How to Balance AI Innovation and Efficiency: Lessons from our 2nd Annual Hypergrowth Engineering Summit

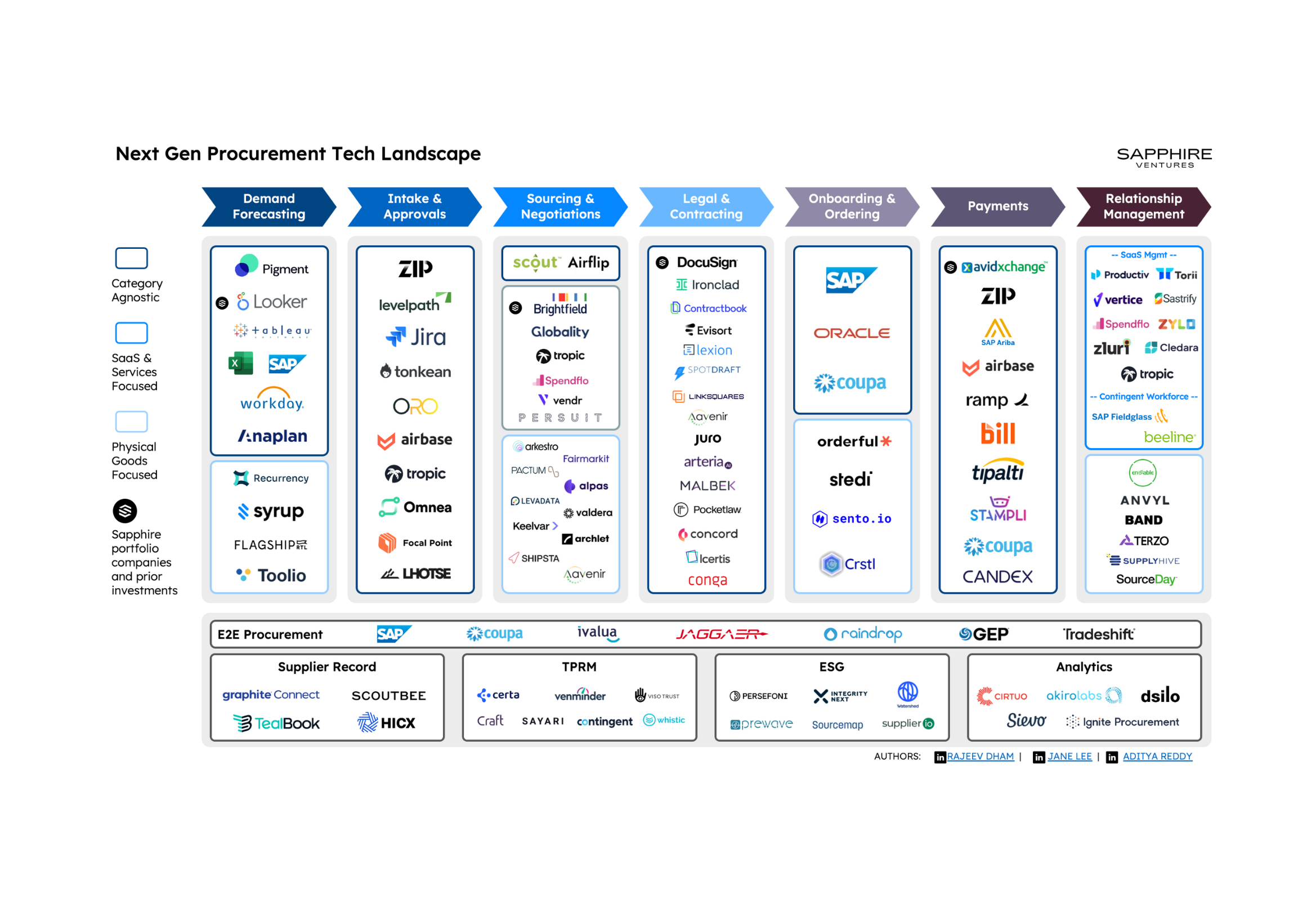

From Purchase Orders to Boardrooms: Procurement’s Tech Renaissance and Evolution

Transitioning from Growth at All Costs to Revenue Efficiency: How to Right-Size Inflated Marketing and Sales Spending

Over the last few years, we’ve witnessed a pervasive trend of growth at all costs. Companies across industries raced to expand their customer base, penetrate new markets and generate rapid revenue growth. While this approach may have yielded short-term gains, it also led to the emergence of unproductive and bloated sales and marketing organizations. The following is a short guide to help organizations transition to a healthier revenue model.

We’ve seen this overexpansion occur in particular around supporting GTM resources. A few examples:

- Sales Development: In an effort to accelerate pipeline generation and take responsibility away from closing roles, we’ve seen the ratio of sales to SDRs draw closer to 1:1.

- Sales Engineering: We have seen an increase in sales engineers (SEs) given the need for more technical overlay roles to support more complex product offerings. In practice, we believe this has led sellers to become overly reliant on SEs early in the sales cycle. As a result, we are seeing sellers spending less time on discovery and learning pain and more time on showcasing features and functionality through demos.

- Customer Success: CS leaders have refined down the “book of business” size for their CSMs to offer more “white glove” support for end customers. While this may be relevant up-market, we are seeing this shift across all segments.

Individually, each of these shifts may not have a significant impact on the efficiency of an organization’s GTM strategy. But in aggregate, we think they lead to highly inefficient revenue organizations.

Let’s walk through an illustration of how this type of GTM strategy can impact a company’s margin for success. Below is a hypothetical “hypergrowth” startup in the first five years of its journey. We applied what we have observed as bloated sales and marketing spend: