AI’s Impact on Venture Capital and Enterprise Software

The 2026 Software x AI Report analyzes how artificial intelligence is reshaping venture capital, public market valuations, and the broader enterprise software ecosystem amid the recent “SaaSmageddon” sell-off. In 2025, global VC investment reached $505B, up 30% year over year, with AI-native companies capturing a significant share of funding and driving record deal concentration. At the same time, public software multiples collapsed to decade lows as investors priced in AI disruption risk. Despite market volatility, many core software fundamentals remain intact, while private valuations, secondary activity, and large-scale M&A have expanded.

Our report’s central thesis: AI is software. Companies that successfully redesign products, pricing, and business models around AI are, in our view, positioned to define the next era of enterprise technology.

To explore the full set of views on the investment and exit environment, download the report here, and read on for key highlights from this year’s report.

The enterprise software landscape has changed dramatically in the last few months as we rapidly traversed the narrative spectrum from “AI is a bubble” to “AI is the destroyer of the entire Software industry.” We believe the truth lies somewhere in the middle. As we like to say: “AI is Software.”

That thesis anchors this year’s Software x AI report. We typically publish this annual report at the end of January, but “SaaSmageddon” interrupted our plans. We have spent the last few weeks recalibrating our outlook to account for the scale and breadth of the recent downturn in public software. Given the scope of this report, this period of reflection was no small task, but one we felt necessary.

AI is posing real disruption risk, both technological and commercial, for certain software categories and companies. At the same time, it is also a massive TAM-expansive force producing some of the fastest growing companies in the history of technology. We believe the reality of the current market environment is that AI is now both the primary bull and primary bear case for software. A company’s ability to leverage AI to reimagine product roadmaps and evolve their business models is now, from our perspective, the most pertinent factor shaping its perception in the capital markets.

As our report seeks to demonstrate, we feel AI is a headwind to public market valuations, which have seen multiples collapse amid fears of displacement risk, while in the private markets, AI is a tailwind. Venture capital is pouring into AI-native companies at an unprecedented pace; investors are betting these will become the era-defining platforms of the next decade. The contrast is stark.

In this year’s report we examine these dynamics through a comprehensive data-backed lens, which we believe is highly relevant to builders, investors, and analysts participating in the enterprise software ecosystem. We have made no predictions this year other than to say that we expect the current period of highly reactionary market volatility to persist. Of course, the crystal ball gets hazy when press releases from the major labs can send entire categories down 10% in a day. Instead of predictions, we focus on several of our favorite views from this year’s report, which we believe capture the most important themes currently defining the investment and exit environment in 2026.

Kicking it off with the private markets:

Theme #1: VC funding accelerates significantly, climbing towards all-time highs

Expand

Sources: PitchBook data pulled as of Dec. 31, 2025; Sapphire internal analysis (Feb. 2026) Notes: PitchBook data is updated on an on-going basis and is therefore subject to change; includes all VC activity for deals with a disclosed transaction size; PitchBook data typically lags public market announcements, resulting in upward revisions to historical figures as new information is captured

levels of concentration

Expand

Sources: PitchBook data pulled as of Dec. 31, 2025; Sapphire internal analysis (Feb. 2026)�Notes: PitchBook data is updated on an on-going basis and is therefore subject to change; includes all enterprise software VC activity for deals with a disclosed transaction size

Deal concentration increased again in 2025 which is unsurprising; the magnitude, however, is staggering. The top twenty enterprise software deals claimed 41% of all funding in the category during the year, and 21% of total funding irrespective of category, while the top five deals accounted for nearly a third of Enterprise Software funding. These are unprecedented levels of concentration as investors plowed even larger rounds into the leading private AI labs.

Several additional trends underscored 2025’s theme of market concentration. Enterprise software investment climbed to 52% of total VC funding. Data, infra, and analytics accounted for nearly 70% of total enterprise software investment, and Series E+ rounds pulled in 28% of capital during the year – each a record by a wide margin. Big rounds got a lot bigger during the year, as $100M+ rounds, several of which went to pre-revenue Seed stage companies, accounted for $164B of investment – also a record.

Theme #3: AI dominates VC investment

Expand

Sources: PitchBook data pulled as of Dec. 31, 2025; Sapphire internal analysis (Feb. 2026)�Notes: PitchBook data is updated on an on-going basis and is therefore subject to change; includes all VC activity for deals with a disclosed transaction size

No surprise here, but it is still helpful to put this dynamic in context. By our strict definition of AI-native funding, investment into the theme rose ~146% YoY to $136B. Others have estimated the figure to be a higher overall percentage of VC funding, with several outlets reporting over 50% of total investment. We believe our approach is a purer expression of truly AI-native funding, but admittedly the boundary between AI-native and AI-augmented is increasingly blurry as it is reasonable to assume that at least a portion of every dollar raised today is going to some form of AI capability. The point is that AI now dominates VC investment.

All layers of the stack saw substantial increases in annual funding in 2025, and while models claimed ~65% of the funding, both the platform and application layer experienced higher relative growth rates. Notably, applications remain far less concentrated, with the top 5 deals coming in under 50% of investment vs. ~85%+ for other layers of the AI tech stack.

The massive quantum of capital deployed by VCs into AI-native companies is supported by strong early performance indicators, as the number of companies reaching $100M, $500M, and $1B in scale continues to expand rapidly. We note over eighty companies, or incumbent products, in the market today that have publicly disclosed clearing the $100M threshold, many of which have done so in under two years of release. Anthropic, which grew from $1B in ARR at the start of 2025 to $14B as of February of this year, has generated the most headlines of late, but the depth and breadth of the AI market continue to improve.

Theme #4: Private market outcomes are larger than ever

Expand

Sources: PitchBook data pulled as of Feb. 18, 2026; Sapphire internal analysis (Feb. 2026) Notes: PitchBook data is updated on an on-going basis and is therefore subject to change; xAI is included at $250B, the valuation assigned at the time of its merger with SpaceX

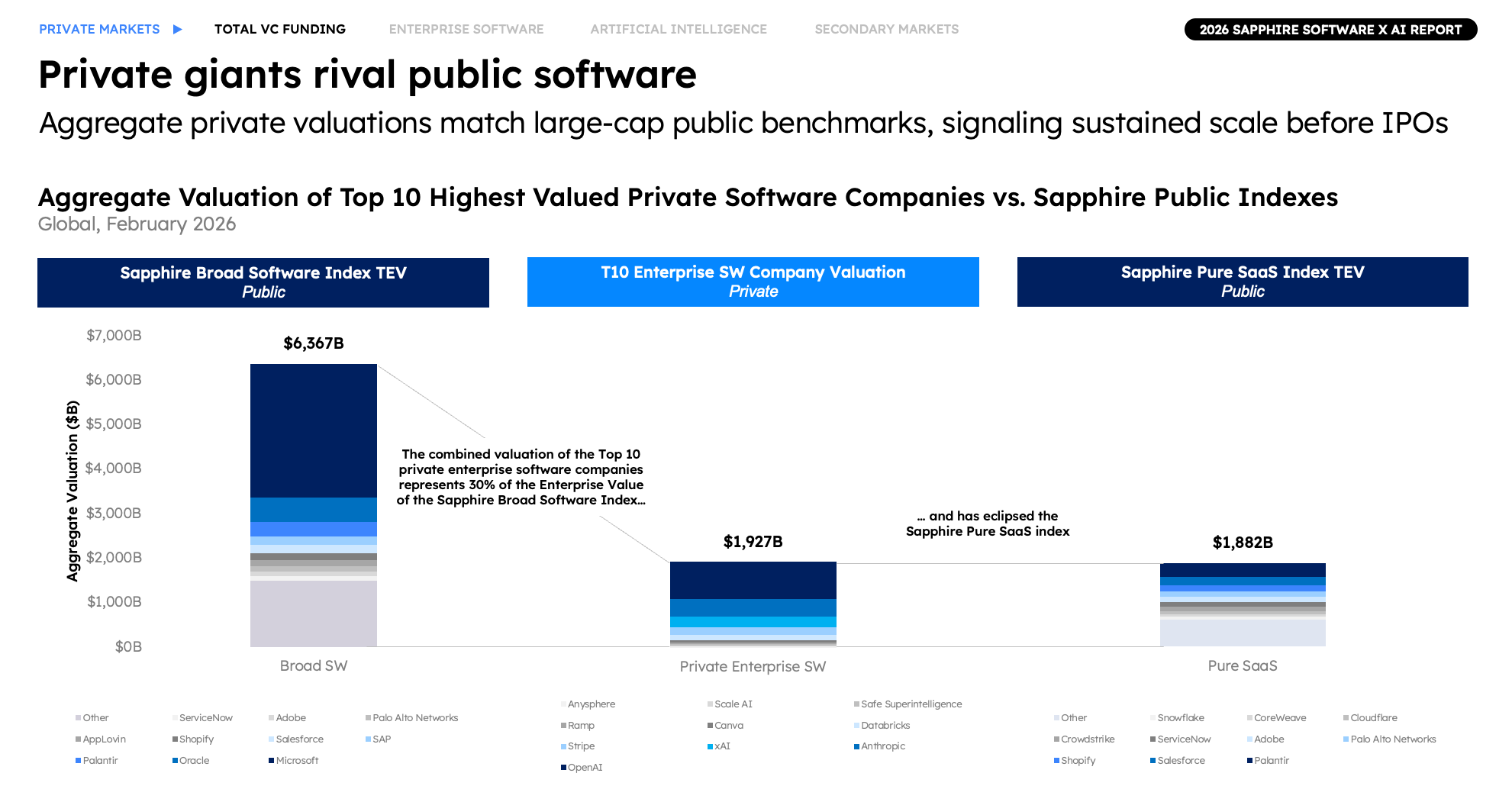

We covered this dynamic in our January 2025 memo, but it’s worth revisiting now. Today’s leading private market companies are larger than they have ever been. The combined valuation of private market enterprise software companies is now over $4.1T, an all-time high that represents 10X+ growth since 2015. Round sizes and median valuations have expanded significantly across every stage over the past decade as companies have sought to stay private for longer, and AI has increased capital requirements to secure compute, model capabilities, and talent.

Today, there are five private companies – SpaceX, OpenAI, Anthropic, Stripe, and Databricks – that stand amongst the fifteen most valuable enterprise software companies in the world (if you allow for a slight stretching of the definition to account for SpaceX now owning xAI).

Need more evidence? The top 10 most highly valued private enterprise software companies carry a combined valuation of ~$1.9T, roughly one-third of the Sapphire Broad Software Index (162 publicly traded software companies, including ~$3T Microsoft) and slightly exceeding the Sapphire Pure SaaS Index (115 publicly traded, subscription-model software companies). When investors and analysts talk about the blurring of public and private markets, this is what they mean.

Theme #5: The secondary market is exploding

Expand

Sources: Campbell Lutyens, '2025 Secondary Market Overview

Secondary market sales more than doubled over the past two years to $225B, as large late-stage companies increasingly used secondaries to give employees liquidity and engage in price discovery ahead of their next primary raise. OpenAI, Anthropic, Databricks, SpaceX, Stripe and Canva were responsible for some of the largest secondary sale offerings ever in 2025 and early 2026, as the practice has now become an increasingly core component of private capital formation.

Looking under the hood at secondary activity based on data from leading private markets platform Hiive, it’s clear that supply of secondary sales continues to outstrip demand, though the gap tightened throughout 2025, falling from a 4x sell-to-buy ratio in April to only a 2x gap in September as demand for hot AI companies came into the market.

Consistent with the narrowing gap, median transaction prices climbed throughout the year, closing 2025 at 66% of last round valuation (vs. a bottom in May of 52%), though there is a very wide range of pricing in a still very opaque market. Encouragingly, the premium paid for the top quartile of companies jumped significantly in the final third of the year, rising to ~130% of last round valuation after hovering around 100% for the most of 2025.

Theme #6: The “SaaSmageddon” in public market software

Expand

Sources: S&P Capital IQ data pulled as of Dec. 31, 2025; Sapphire internal analysis (Feb 2026) Notes: Sapphire Broad Software Index includes 252 Sapphire-selected companies, 162 of which are currently public; Sapphire Pure SaaS Index includes 179 Sapphire-selected companies, 115 of which are currently public

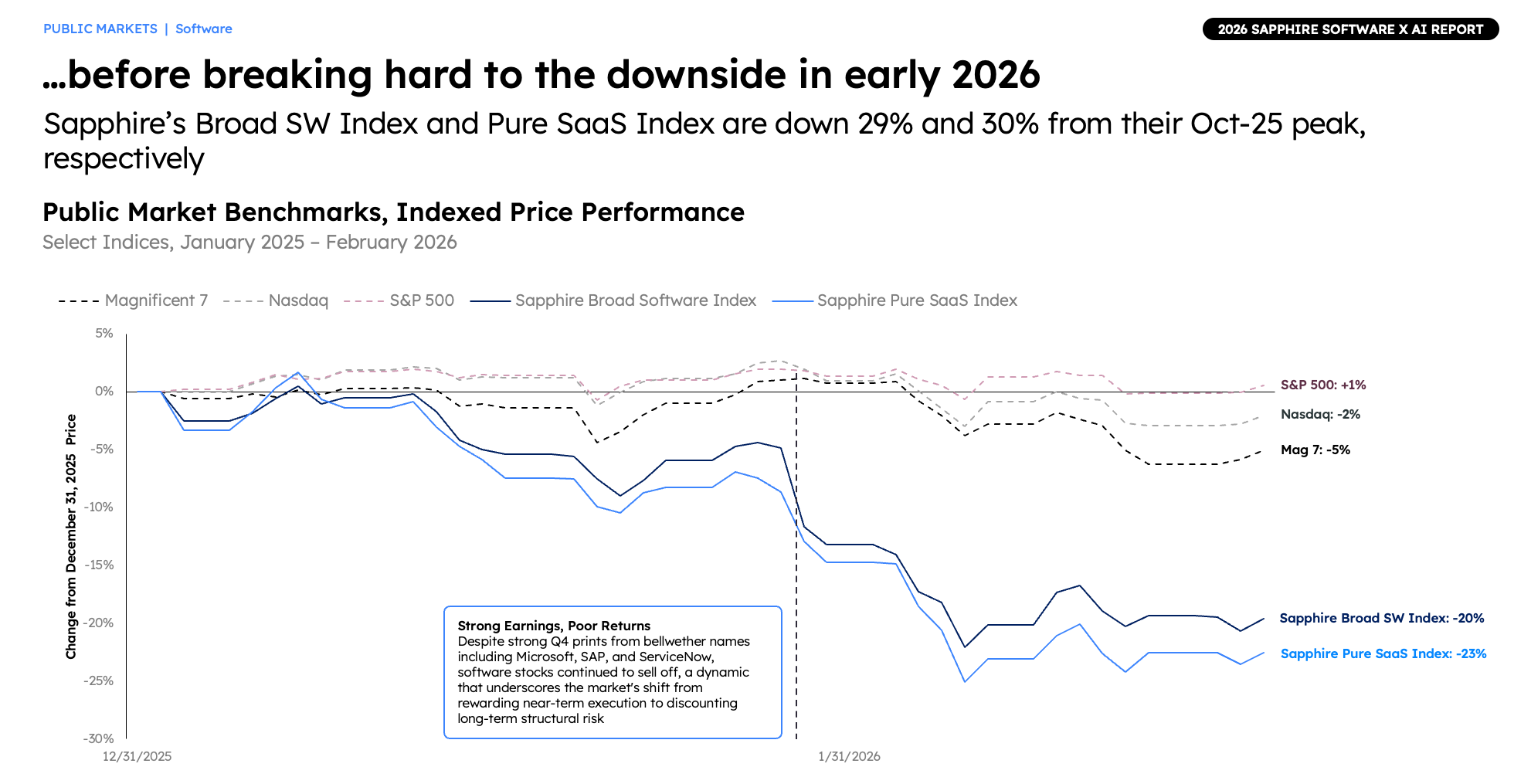

Where to start? Our Sapphire Broad Software Index (+10%) and Pure SaaS Index (+7%) saw gains in 2025, building incrementally on a strong second half of 2024, though they underperformed major benchmarks (Nasdaq +21%, S&P 500 +16%) and the Mag7 (+22%). While the public discourse around software stocks intensified in late January 2026, valuations peaked in October 2025 and steadily declined before more pronounced selling early this year.

Expand

Sources: S&P Capital IQ data pulled as of Feb. 18, 2026; Sapphire internal analysis (Feb. 2026) Notes: Sapphire Broad Software Index includes 252 Sapphire-selected companies, 162 of which are currently public; Sapphire Pure SaaS Index includes 179 Sapphire-selected companies, 115 of which are currently public

The numbers are sobering. In 2026 so far, our broad Software Index is down 20% through February 18, while the Pure SaaS index has declined 23%. Selling has been indiscriminate, pulling down all sub-categories and sparing none of 2025’s most favored companies. It’s ugly out there.

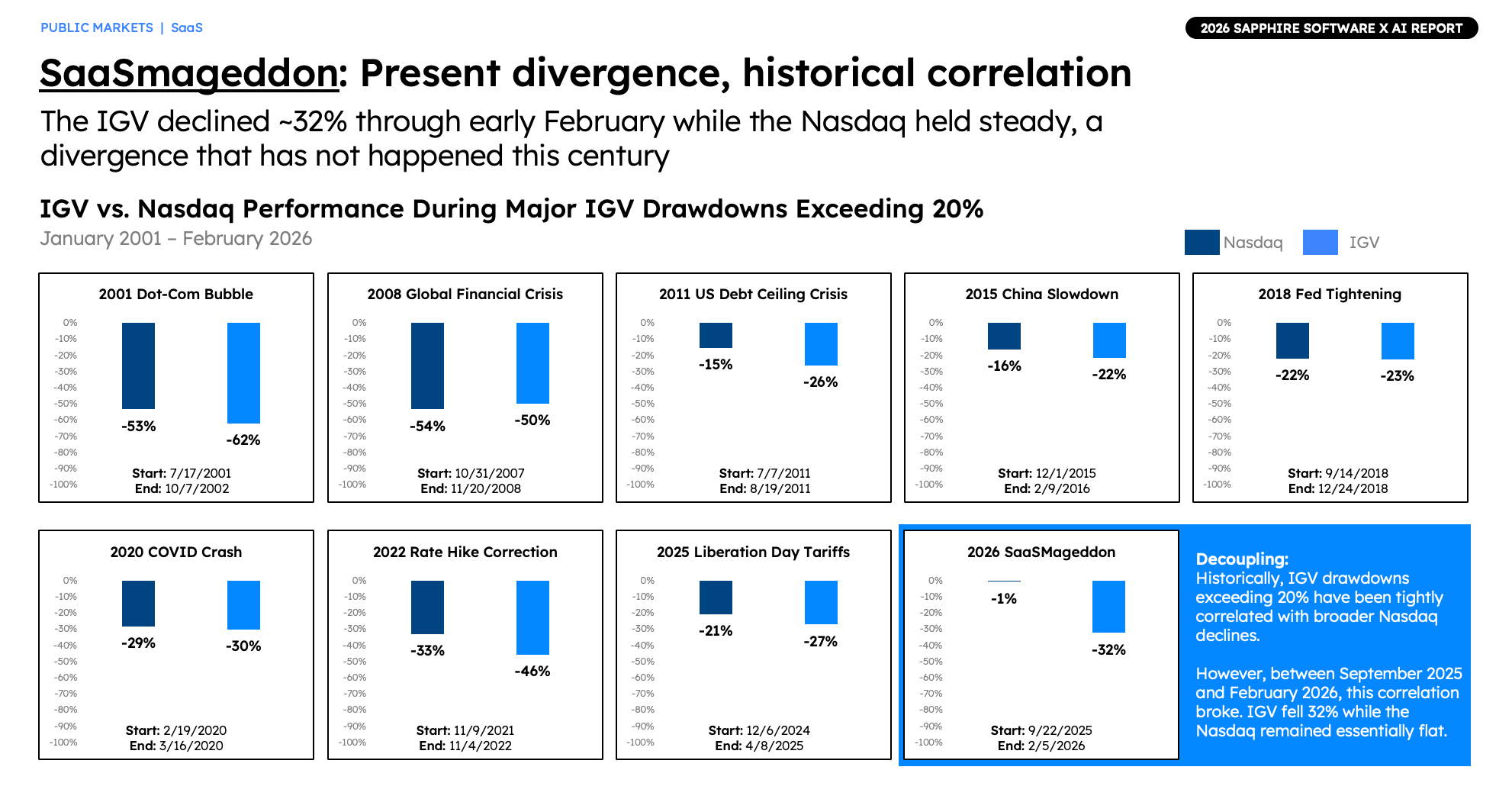

We looked at every significant drawdown in software since 2000, using the IGV index as a proxy, and identified nine instances in which the sector declined 20% or more over that period. What stands out is that in every other instance, IGV moved in close sync with the Nasdaq, whereas in this instance, IGV is down 32% as the broader index is essentially flat.

Expand

Sources: S&P Capital IQ data pulled as of February 18th, 2026

Why is this the case? There are several convergent factors at play:

- Growth rates for public software companies have been in decline for 5 years, falling from a median of 31% in 2021 to 11% expected in 2026, emblematic of a much more mature (vs. hypergrowth) public market.

- Technology budgets are now shifting towards AI initiatives, pulling more spend away from incumbent (non-AI-native) software companies.

- Business models are evolving to more tightly align pricing to consumption of measurable value delivered, which acutely hits certain seat-based dominant categories such as GTM software which are public market bellwethers.

- AI products from incumbent companies, while growing fast in many cases, are not yet material enough to drive performance of their overall business, much less assuage fears of displacement by AI-native startups.

- Continuous performance gains in AI models are increasing the displacement risk for established incumbents, raising questions about long-term competitive positioning.

Taken together, we believe investors are selling first and asking questions later, putting the onus on companies to prove themselves as AI beneficiaries over the next several quarters. If you are not an AI winner, you are effectively treated as an AI loser. In short, risk is up, and terminal value assumptions are down (for now at least).

Theme #7: Public market software multiples have collapsed

Expand

Sources: S&P Capital IQ data pulled as of Feb. 18, 2026; Sapphire internal analysis (Feb. 2026) Notes: Sapphire Broad Software Index includes 252 Sapphire-selected companies, 162 of which are currently public; Sapphire Pure SaaS Index includes 179 Sapphire-selected companies, 115 of which are currently public; COVID years defined as March 2020 – March 2022; data based on mean consensus NTM revenue estimates; data pulled as of the last day of each month

Aren’t we done talking about the SaaSmageddon yet?! The air coming out of valuations to date has primarily been a function of pressure on multiples vs. fundamentals (more below), as investors look ahead to mid-to-long-term disruption risks. We thought coming into the year that software stocks would recapture the 10-year average of 5.9x EV/S and at the start of the year it looked like we were going to be correct. The trend did not hold.

As of February 18, the median multiples for both our Broad Software and Pure SaaS index stand at 3.1x EV/S, decade lows for both. They have each collapsed ~40% YoY, and are down 72% and 80%, from their respective cycle peaks. The impact has been across the board as both the growth premium and scale premium in multiples have fallen well below 10-year averages as well. Even Palantir, coming off one of the most impressive quarters in enterprise software history, saw its NTM revenue multiple retrace from 72.9x to 43.7x between year-end 2025 and February 18, 2026.

Theme #8: Software metrics are holding up well

Expand

Sources: S&P Capital IQ data pulled as of Dec. 31, 2025; PublicComps.com; company filings; Sapphire internal analysis (Feb. 2026) Notes: Sapphire Pure SaaS Index includes 179 Sapphire-selected companies, 115 of which are currently public; 2025 NDR and magic number data as of last public filing; magic number shows LTM average of current quarter net new ARR/prior quarter sales & marketing expense; FCF calculated as CFO – capex; * represents current or former Sapphire Ventures portfolio company

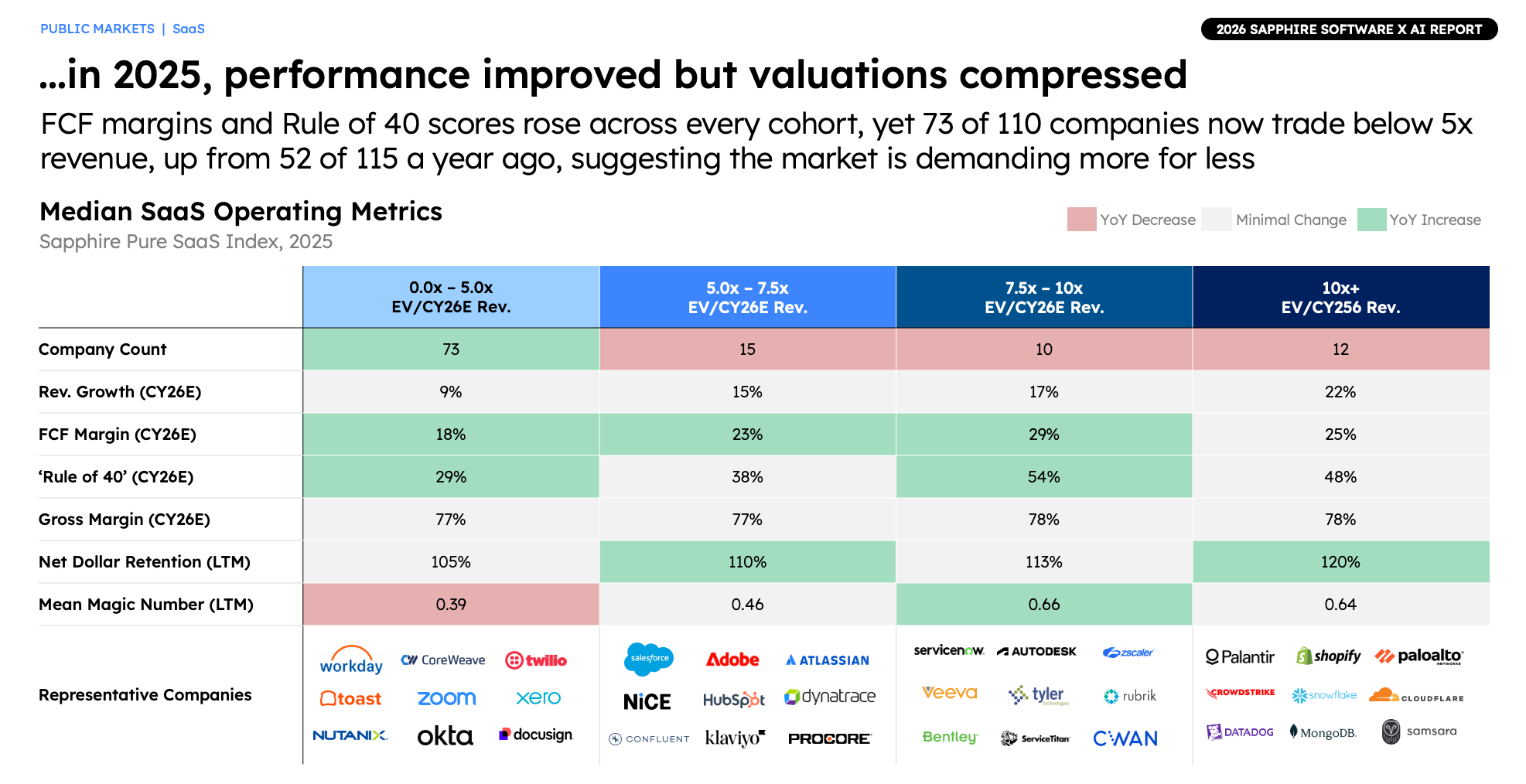

As we have already discussed, median growth in public market software has been in decline for years, and investors are still overweight growth when assessing public market software stocks. There’s no getting around this crucial factor. However, many other metrics have held up well or incrementally improved in the face of this current drawdown. Median gross margins ticked up again in 2025, non-GAAP free-cash-flow (FCF) margins improved (putting pesky SBC costs aside), NDR ticked up after declining for the previous three years, and “Rule of 40” was solid, if not spectacular. Sales efficiency did tick down again, extending a worrying trend.

The current operating picture is not bleak, but it is not what matters. Markets are forward looking, and many investors appear to view incremental improvements as insufficient in an era of AI acceleration. Investors are demanding more evidence that AI investments are driving stronger top and bottom-line performance.

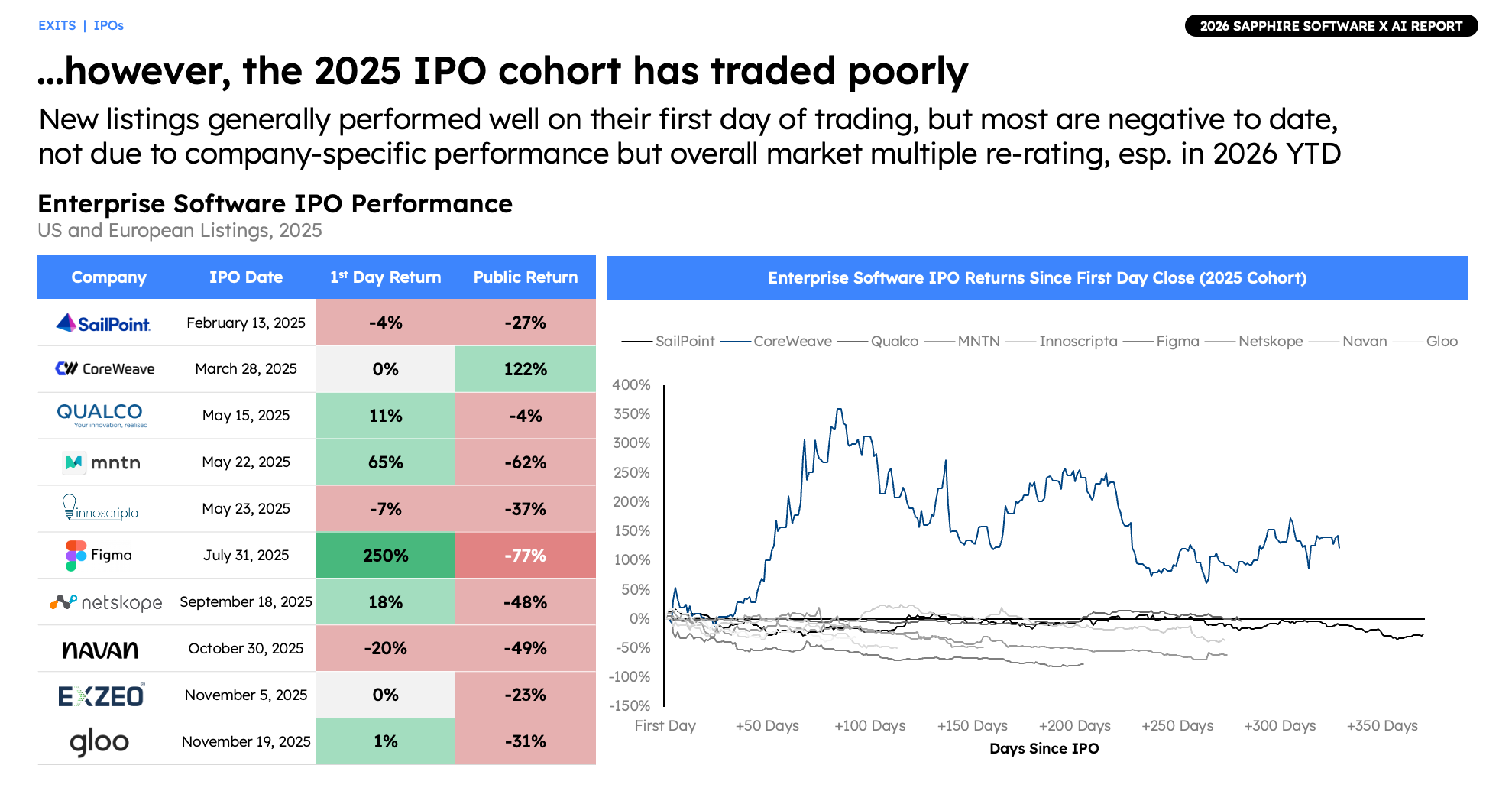

Theme #9: IPOs: Tough debuts, big, but concentrated, 2026 potential

Expand

Sources: S&P Capital IQ data pulled as of Dec. 31, 2025; Sapphire internal analysis (Feb. 2026) Note: IPO data includes all enterprise software IPOs listed on US and European exchanges

The IPO window opened modestly in 2025, with ten enterprise software listings raising $7.1B in gross proceeds, roughly double 2024 levels but still well below the 10-year average of fourteen new issues per year. As discussed above, we believe ample VC funding and an extremely healthy secondary market are among the factors making it easier for companies to stay private for longer.

The performance of new issues is also likely not a motivating factor for potential IPO candidates. After some promising first-day returns, overall performance for the 2025 cohort has been poor, with most now trading below their first-day close. The early 2026 market selloff will likely complicate the IPO calculus for many firms, with only the most capital-intensive businesses looking like candidates to go out this year.

We feel this year will likely be defined by historically large IPOs, with SpaceX, Anthropic, and OpenAI each reportedly considering listings at valuations approaching or exceeding $1T. If each company does follow through with rumored plans, we will see three of the four largest IPOs ever over the next 10 months. We also feel it will likely be another year of very restrained activity as companies that meet today’s higher scale and growth bar for IPOs (e.g., Stripe, Databricks and Canva to name a few) will be apt to seek more favorable market conditions before moving forward into 2027 or beyond.

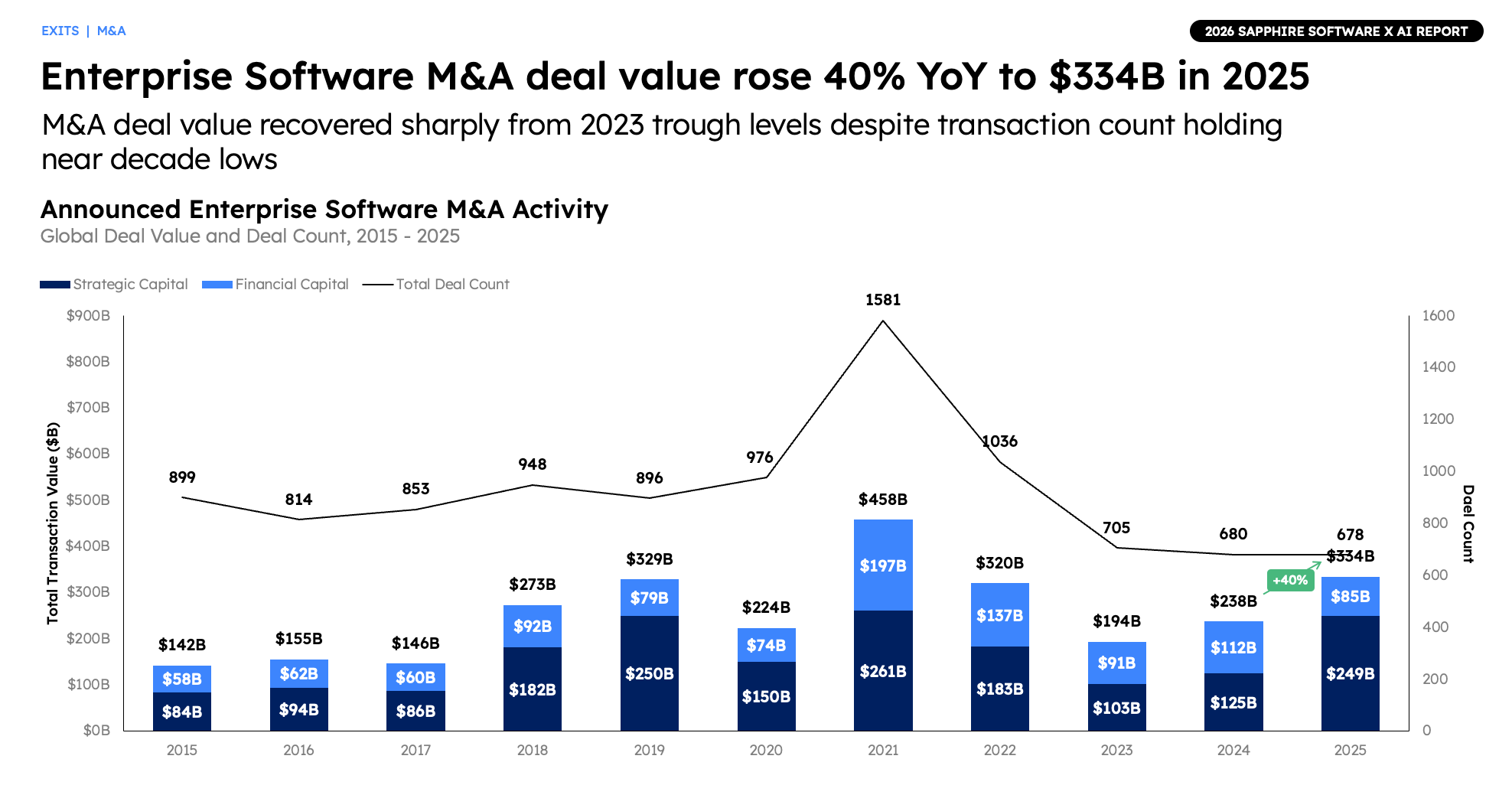

Theme #10: M&A: A hot market that should remain strong

Expand

Sources: PitchBook data pulled as of Dec. 31, 2025; Sapphire internal analysis (Feb. 2026) Notes: PitchBook data is updated on an on-going basis and is therefore subject to change; includes all enterprise software M&A activity for deals with a disclosed transaction size; deals sorted by announced date

Software M&A activity picked up meaningfully in 2025, with announced deal value rising 40% YoY to $334B across 678 transactions. Security was a leading theme, led by Google’s $32B acquisition of Wiz, Palo Alto Networks’ $25B bid for CyberArk, and ServiceNow’s $7.8B deal for Armis. Several software incumbents, including Palo Alto, IBM, ServiceNow, Siemens, Workday and Salesforce, bought three or more companies during the year as they leaned into inorganic growth to accelerate AI product roadmaps and complement core platform offerings. Notably, the median multiple for $1B+ acquisitions fell again to 5.5 EV/NTM, across the 16 transactions in which data is publicly available. This is the 3rd lowest median multiple paid in the 2015—2025 period, and current sentiment around software valuations likely keeps pressure on pricing

While the big deals get most of the headlines there has been a lot of smaller strategic activity of late, both with late-stage private-to-private mergers (e.g. DBT Labs + Fivetran, Seismic + Highspot) and with AI-natives (e.g., Anthropic + Bun and Vercept, OpenAI + Neptune, Statsig, and Torch.ai). We expect this trend to continue in 2026, as late-stage companies seek to add the scale required to reach IPO candidacy and AI-Natives seek to use their record funding to extend advantages.

Looking Ahead

Though the current market narrative may be skewing more towards the doomer view of category, we continue to believe Software is alive and well. After all AI is software. We believe we have moved past experimentation into the first phase of economy-wide adoption. As with all previous platform shifts, this one will create a new class of winners and losers, but ultimately AI is a massively TAM expansive force that will significantly grow the global software market in the decades to come. The companies that can best leverage the technology to reimagine product experiences, business models, and operations will be well positioned to lead in the AI era.

The real test has begun.

Sign up for our newsletter

Legal disclaimer

Nothing presented herein is intended to constitute investment advice, and under no circumstances should any information provided herein be used or considered as an offer to sell or a solicitation of an offer to buy an interest in any investment fund managed by Sapphire Ventures, LLC (“Sapphire”). does not solicit or make its services available to the public. Prospective investors may rely only on a fund’s confidential private placement memorandum or an official supplement thereto. An investment in a Sapphire fund is speculative and involves a high degree of risk.

Information provided reflects Sapphires’ views at a point in time. Such views are subject to change without notice; as of February 18, 2026 unless otherwise noted.

Certain information contained in this presentation including any prediction or projection may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “target,” “project,” “estimate,” “intend,” “continue” or “believe,” or the negatives thereof, or comparable terminology. Due to various risks and uncertainties, actual events or results, or the actual results may differ materially from those reflected or contemplated in such forward-looking statements, and no assumptions should be made that any such strategy or investments were or will be profitable. Sapphire provides no assurance or no guarantee that any such prediction will ultimately occur.

This Presentation has been prepared from original sources, or other cited data, and is believed to be reliable. However, no representations are made as to the accuracy or completeness thereof. The information in this Presentation is not presented with a view to providing investment advice with respect to any security, or making any claim as to the past, current or future performance thereof, and Sapphire expressly disclaims the use of this Presentation for such purposes. The inclusion of any third-party firm and/or company names, brands and/or logos does not imply any affiliation with these firms or companies. None of these firms or companies have endorsed Sapphire or its affiliates. References to specific companies in this Presentation are for illustrative purposes only and should not be considered a recommendation to carry out securities transactions. It should not be assumed that recommendations made in the future will be profitable or will equal the performance discussed herein.

“Internal Sapphire Analysis” described within respective graphs above refers to observations of the ”Sapphire Internal Public SaaS Index” which is an internal paper composite maintained by Sapphire is for informational purposes only and is in no way intended to constitute investment advice. The index consists of individual SaaS related public equities chosen at Sapphire’s discretion. The index is not investable and does in no way represent any investment offering to be made in any fund managed by Sapphire. While Sapphire has used reasonable efforts to present observations from analysis of the index, Sapphire makes no representations or warranties as to the accuracy, reliability, or completeness of observations presented within any analysis described or the index itself. All metrics and observations described in relation to the index must be considered academic and hypothetical in nature and are in no way guaranteed in actual practice. While Sapphire has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability, or completeness of third-party information presented within the index or this article. No assurance can be given that all material assumptions have been considered in connection with the analysis of the index, therefore actual results may vary from those estimated therein and are subject to change. No assumptions should be made that any investments described above were or will be profitable.

The content in this Presentation has not been reviewed or approved by the Securities and Exchange Commission.

Past performance is not indicative of future results.