The thing that hides them is the same thing that makes them defensible.

The biggest opportunities in vertical AI are hiding in markets most founders would never touch.

They’re fragmented, operationally messy, and full of edge cases. The workflows are painful. The buyers are hard to reach. Nothing about them screams venture-scale opportunity.

That’s the trojan horse.

Over the past two years, vertical AI has been one of our highest-conviction themes at Sapphire. We’ve backed companies across healthcare, legal, housing, and financial services, and we’ve seen hundreds more pitches.

The surface pattern is strikingly consistent: better demos, faster deployments, a path to $5-10M ARR quicker than any generation of software before. But the companies are splitting into two very different trajectories.

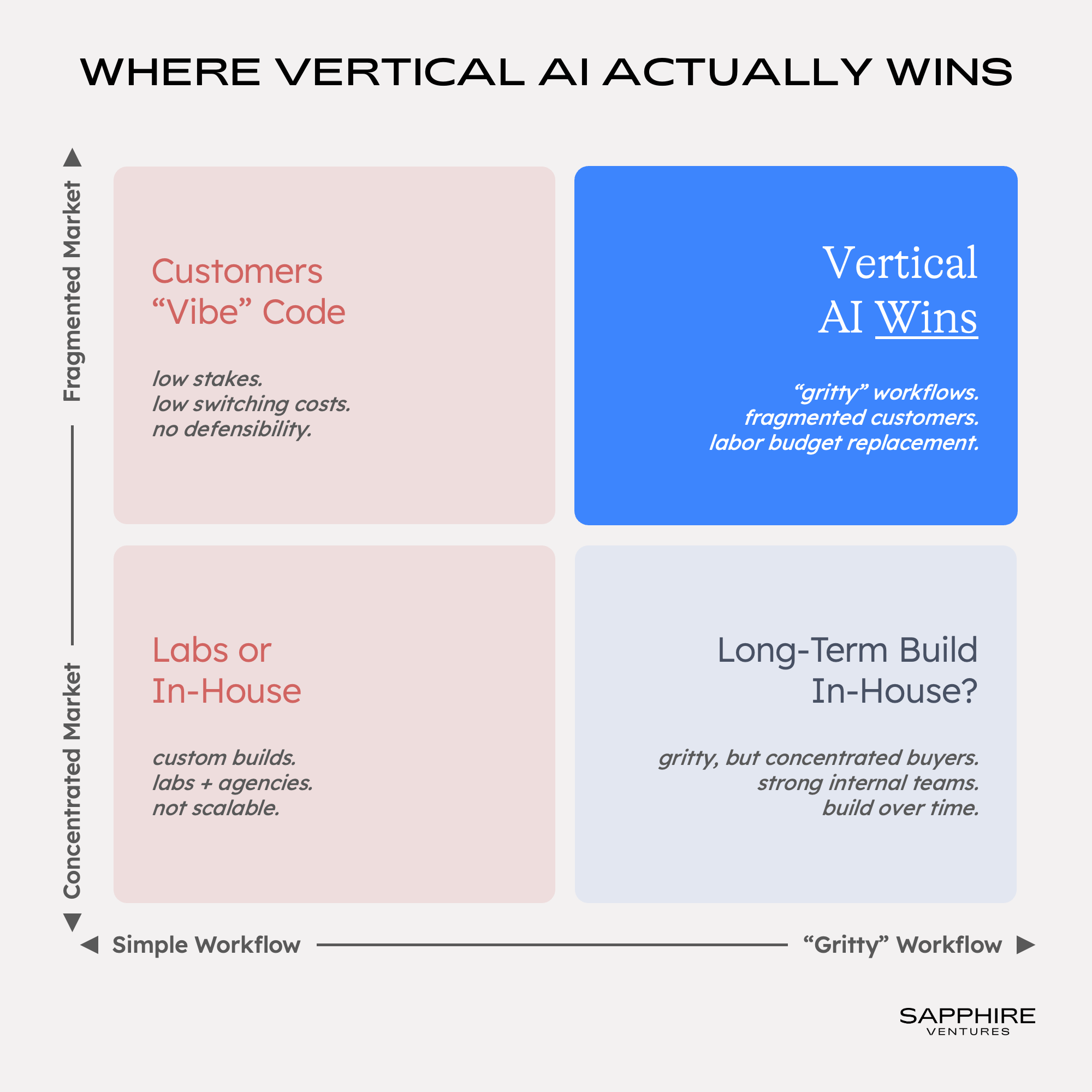

One group builds a vertical AI product: intelligence injected into a task. The other builds a vertical system: the data, integrations, approvals, exceptions, compliance layer, and eventually the labor budget behind the work, owned end to end.

We think the next generation of $10B+ vertical AI systems are going to be built in markets that everyone else overlooked.

Why These Markets Stay Hidden

Two qualities keep the best vertical AI markets hidden, and they’re the same two qualities that make those markets defensible once you’re inside them.

The first is workflow grit.

The best markets are full of exceptions, legacy integrations, human approvals, compliance requirements, and expensive failure modes. The work is messy, and messy work resists abstraction. Clean, well-defined tasks are where most vertical AI companies start, and for good reason, as they’re easier to build, demo, and sell. But they’re also structurally harder to defend, because clean workflows get commoditized the moment intelligence becomes portable. If the job is narrow, low-risk, and easy to slot into existing systems, a competitor can copy the feature, a customer can build it, or a frontier lab can ship it directly.

Gritty workflows repel all three threats. Labs don’t want to handle the operational mess. Customers lack the technical capacity. Competitors can’t shortcut the work. The grit is what hides the market. It’s also what makes the market defensible.

When a company has to make AI usable inside a gritty workflow, it builds far more than model access. It structures messy data, integrates with old systems, designs approval loops, defines acceptable error rates, and wins trust where mistakes are costly. That work compounds quietly into something no new entrant can replicate by buying the same model. It becomes a proprietary map of how the workflow actually runs, built from every edge case handled, every integration maintained, every workaround encoded.

The hard operational effort for what initially seems like a modest reward, is what earns the company the right to expand into adjacent workflows and increasingly large budget categories over time.

Consider what “AI for auto lending” looks like in practice. Salient builds AI voice agents that call borrowers about overdue car payments, a workflow governed by FDCPA, TCPA, and Reg F, where a single violation can trigger regulatory action. The AI has to navigate overlapping state and federal rules, handle payment negotiations in real time, comply with call frequency limits, and route exceptions to human agents when needed. This is not a single task but a messy collection of operational, regulatory, and technical problems that offer less obvious leverage than broader, more horizontal opportunities. But auto lending servicing is a massive market, and the unit economics are dramatic. A human collections call costs $4-$12, while an AI call costs a fraction of that.

You see the same dynamic in medical billing, where Charta Health automates pre-bill chart review across overlapping payer rules, CPT codes, and denial patterns that vary by specialty and geography. And in freight logistics, where companies like HappyRobot, Pallet, and Augment are building AI agents that handle the endless voice calls, emails, and portal updates required to coordinate carriers, shippers, and warehouses. “Calling truckers about load status” doesn’t sound like a venture-scale opportunity until you realize that every load involves dozens of manual touchpoints, and the logistics industry spends over a trillion dollars a year on non-physical operational costs. The grit is what keeps these markets overlooked and makes them more challenging to pursue than they first appear.

The second is market structure.

These markets are fragmented across thousands of operators, and the buyers often have low tech DNA. That combination shapes who can realistically serve them.

Horizontal AI vendors need concentrated, high-value customers to make deployment economics work. When the revenue is spread across thousands of small and mid-sized operators running different systems on messy data, a generalized player can’t justify the go-to-market effort. But a purpose-built vertical system, willing to do the hard work of going market by market, can make those economics work.

Building AI in-house requires engineering teams, architecture opinions, and the instinct to treat technology as something you own rather than something you buy. Real estate operators, field services companies, and outpatient rehab clinics typically do not have those capabilities in-house. Some of these buyers are sizable companies, but they lack the technical DNA to build production AI on their own. That makes them natural customers for a vertical system that arrives ready to do the work.

Fragmentation creates a window to build. Low build instinct widens it. Together, they give vertical AI companies the room to compound operational context before anyone else shows up.

We believe the U.S. tax and accounting market illustrates this well. It is a $145 billion industry with a long tail of roughly 46,000 CPA firms, 86% of which have fewer than 10 employees, but it also includes the Big Four and large national practices with real technical sophistication. Blue J*, an AI-powered tax research platform, has found traction across both ends, now serving 2,800+ organizations with usage growing 700%+ year over year. The long tail makes the market unattractive for generalized players to chase, while the workflow grit–overlapping tax rules, ambiguous fact patterns, and answers professionals stake their reputation on–makes the wedge durable even with demanding buyers.

The moat is built around work no one wants, in a market that’s hard to chase, for buyers who will never build it themselves.

When both forces combine, the result is a compounding head start that’s very difficult to close. The operational complexity creates switching costs that make removal highly disruptive–requiring companies to hire people back, rebuild processes, and give up years of accumulated workflow context. The fragmentation doesn’t get less fragmented over time. The buyers don’t suddenly develop engineering DNA. And by the time the market is visible enough to attract attention from OpenAI or Anthropic, the vertical system’s operational context and distribution footprint have years of compounding behind them.

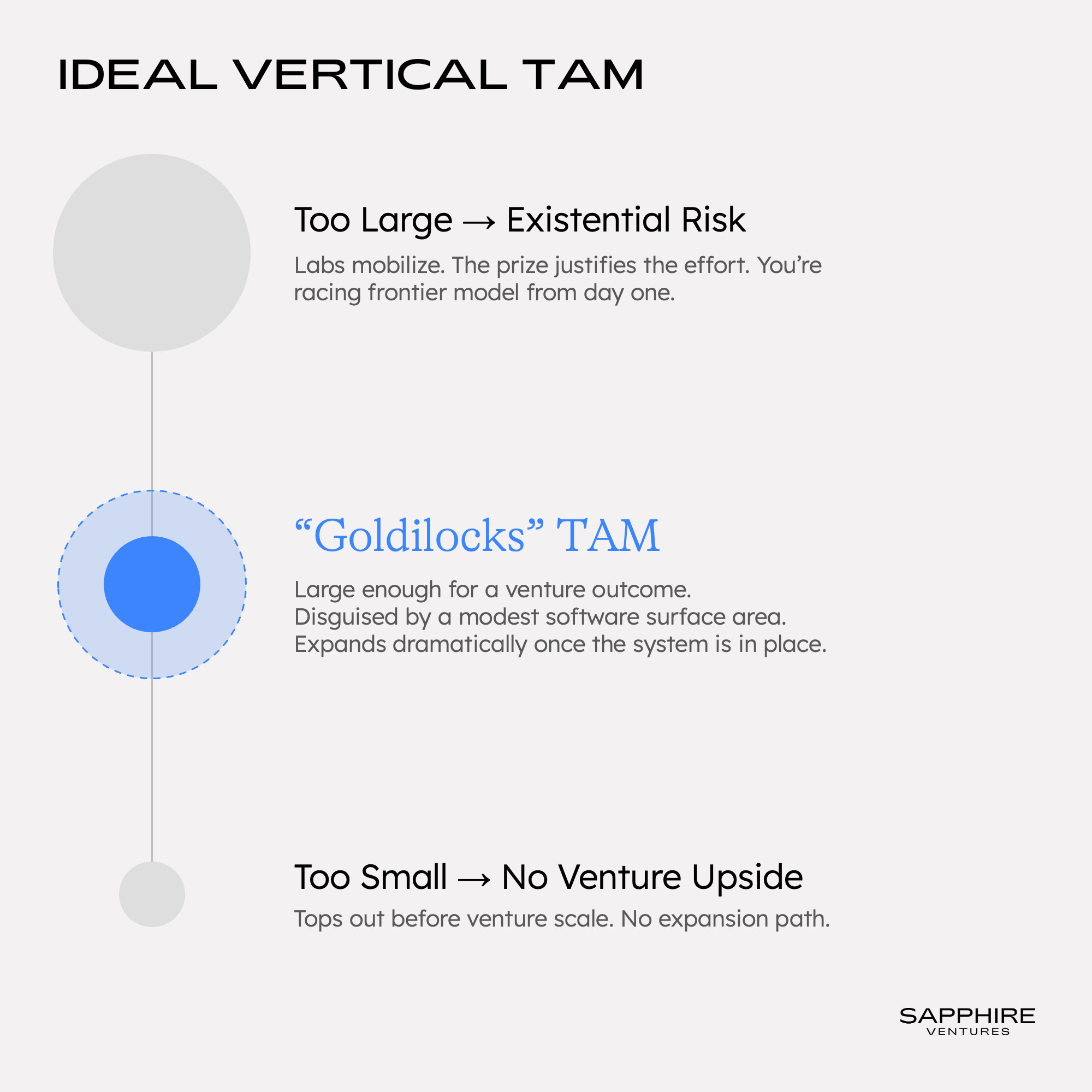

The Goldilocks TAM

We think the biggest vertical AI markets stay hidden because everyone sizes them wrong.

The standard approach is to look at what customers spend on software in a category and call that the TAM. By that measure, most vertical AI markets look small, because the software budgets in fragmented, operationally messy industries tend to be modest. But software spend is the wrong denominator. In these markets, the real money sits in services and labor: the people doing the work, the outsourced providers handling the overflow, the agencies and contractors filling the gaps. The right way to size a vertical AI market is to ask what the industry spends on the work itself, not on the tools.

That reframing also explains why these markets stay overlooked by the most dangerous competitors. If you size “AI for property leasing” by the software budget, it looks like a niche. No frontier lab is going to mobilize around a niche. If you size it by the labor and services budget, it’s enormous, but by the time that’s visible, the vertical system has already been compounding for years. Markets that look too big and too obvious from the start attract labs directly, because the prize justifies the effort. The Goldilocks TAM is large enough for a venture outcome but disguised by a modest software surface area, operationally messy enough to be overlooked, and capable of expanding dramatically once the system position is established.

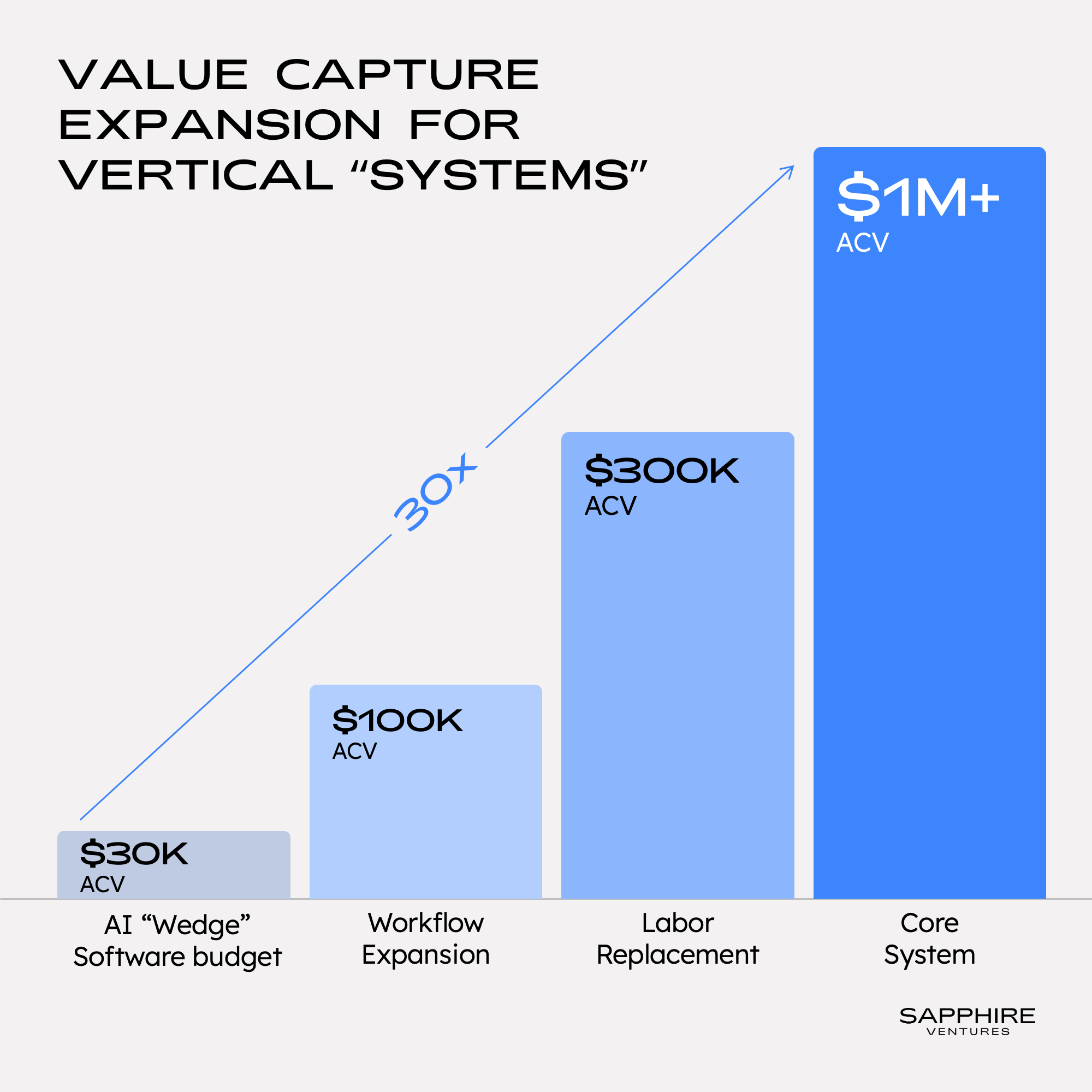

The expansion happens when the product shifts from assisting the work to doing it. Consider what that means at the level of a single customer. A property management company might spend $30,000 a year on leasing software. It spends $300,000 on the leasing staff. The moment the product starts doing the work, you’re no longer selling into the $30K line item. You’re selling into the $300K one. And as the product expands across more of the workflow and operations, you begin to access the full operating budget, which can be $1M or more per account. Same customer, same company, 30x expansion in addressable spend, simply by going deeper.

Expand

Note: ACV figures above are illustrative and represent the potential for value capture expansion as vertical AI companies evolve into vertical “system” companies.

EliseAI*, an AI property management platform, shows what this looks like at scale. What appeared to be a bounded proptech market with Elise’s single SKU leasing automation solution starting at a ~$50K ACV ultimately expanded the moment the product replaced leasing work rather than assisted it, then expanded further into maintenance, collections, and AI-guided tours across the tenant lifecycle. Today, Elise serves 1 in 8 U.S. apartments with property managers/operators spending well into the millions for the platform and the company has also moved into healthcare, targeting $600 billion in annual administrative costs with the same playbook. The TAM didn’t grow with the product. The product revealed how large the TAM always was.

What Happens When You Get There First

The vertical AI companies that reach system position in these markets won’t just build big businesses. They’ll define how entire industries operate for the next decade.

Not every market will play out this way. Some companies will win in concentrated markets by moving faster than anyone expected. Others will build durable positions on intelligence wedges that prove harder to copy than they initially appear. And while Anthropic and OpenAI pose real risk to the application layer, they are also juggling conflicting priorities. They must perpetually invest to advance the model frontier. They must maximize token-based revenue, which runs at odds with end customers as agent adoption scales. And on top of all that, they would need to build high-quality, bespoke applications for dozens of different verticals simultaneously. In most markets, purpose-built vertical AI will win by out-executing the labs through sheer focus. But when we look at the companies that have built real system positions, the combination of gritty workflow, fragmented market, and expanding surface area shows up again and again.

The next five years will determine which approach wins in each market: purpose-built platforms that expand an AI wedge into a vertical system, incumbent system-of-records that layer on “good-enough” AI to retain market position or bespoke AI built “in-house” on top of Anthropic/OpenAI. The race is already underway.

Pick a sharp, operationally messy wedge in a market that looks too small to matter. Expand across the workflow as you earn the right. Displace labor. Become the system the customer can’t run without.

Models win demos. Wedges win pilots. Systems win markets.

If you’re building in a hidden vertical AI market and the above resonates, reach out, we’d love to hear from you: Cathy ([email protected]), Adi ([email protected]).

Sign up for our newsletter

Legal disclaimer

* Denotes a Sapphire portfolio company.

This article is for informational purposes only. Nothing presented within this article is intended to constitute investment advice, and under no circumstances should any information provided herein be used or considered as an offer to sell or a solicitation of an offer to buy an interest in any investment fund managed by Sapphire. Information provided reflects Sapphires’ views as of a time, whereby such views are subject to change at any point and Sapphire shall not be obligated to provide notice of any change. Companies mentioned in this article are a representative sample of portfolio companies in which Sapphire has invested in which the author believes such companies fit the objective criteria stated in commentary, which do not reflect all investments made by Sapphire. A complete alphabetical list of investments made by Sapphire’s Growth strategy is available here. No assumptions should be made that investments listed above were or will be profitable. Due to various risks and uncertainties, actual events, results or the actual experience may differ materially from those reflected or contemplated in these statements. Nothing contained in this article may be relied upon as a guarantee or assurance as to the future success of any particular company. Past performance is not indicative of future results.