It shouldn’t take 15 years and 2 billion dollars to bring a new therapy to patients.

Pharma has known for decades that drug development is too slow, too expensive and too failure-prone. Roughly 90% of clinical trial candidates fail. Of the 10,000+ diseases that exist in the world, just over 600 have an approved drug treatment. The industry has spent hundreds of billions trying to make the science better.

But the more interesting insight is that drug development is not only a science problem. It is an operating model problem.

Underneath the biology, pharma is a massive services industry.

Clinical research organizations (CROs) run trials. Regulatory consultants draft submissions. Field teams educate physicians. Medical affairs agencies create content. Quality specialists review deviations. Manufacturing teams document batch records. Bioanalytical labs process samples. Patient support teams chase prior authorizations and benefits checks.

For decades, this model was the only model. The work was judgment-heavy, fragmented and highly regulated, all of which made it difficult to encode in software. So the pharma industry outsourced the complexity to people. The result was a drug development stack where the most important operational workflows were not software-native.

AI changes this.

For the first time, software can read the literature and reason across heterogeneous data to do things like generate regulated documentation and even design molecules.

Over the past 18 months, we’ve spent time mapping the AI-native life sciences landscape, talking with founders and operators across the stack, and developing a view on where durable companies are emerging. We believe the real venture opportunity in AI life sciences lies in the emergent software layer that will absorb the operational labor behind how every therapy moves from hypothesis to patient.

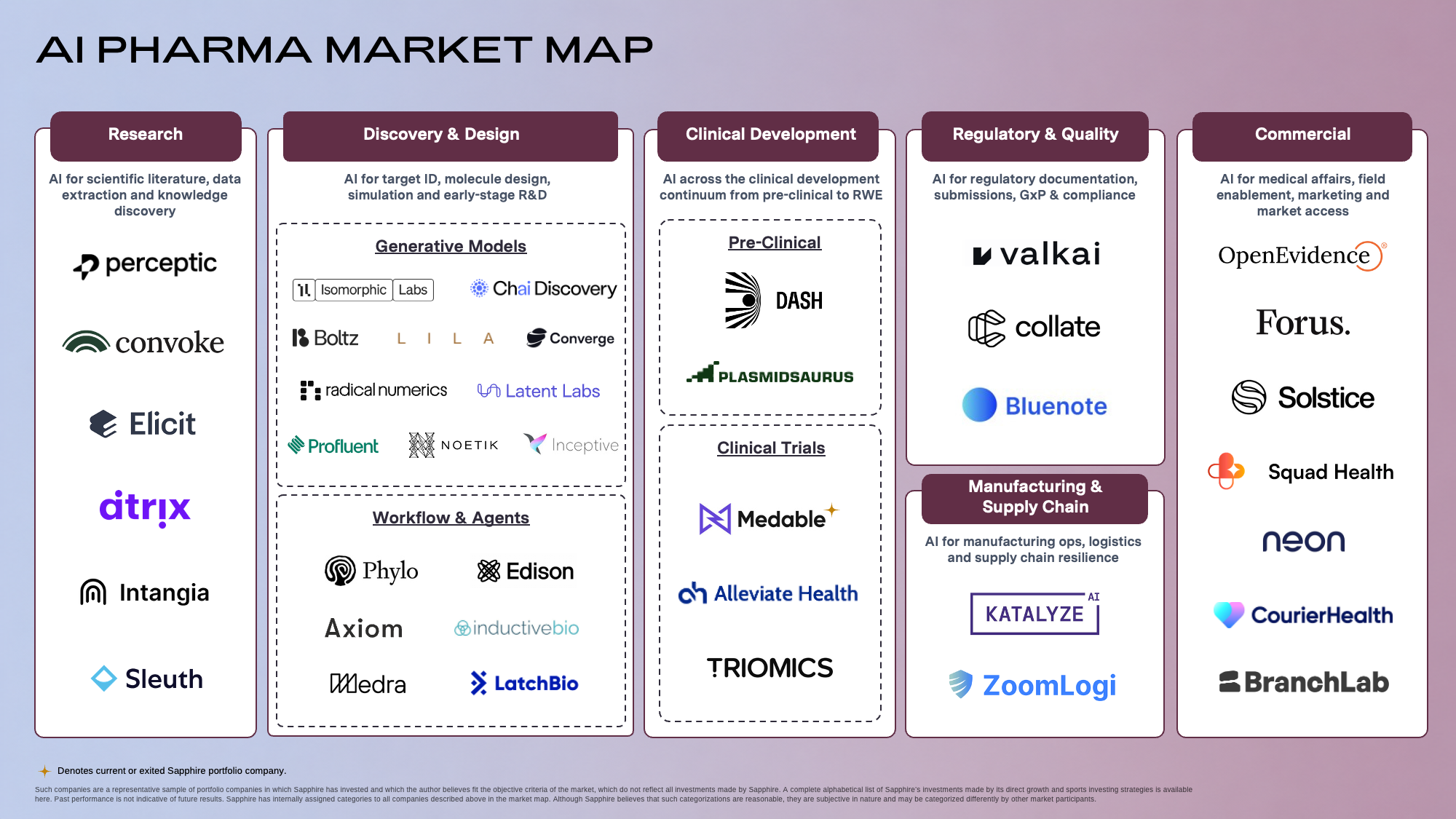

The opportunity is far broader than the “AI for drug discovery” narrative that dominates most of the conversation. AI is now entering every layer of the drug development lifecycle, spanning scientific research, molecular design, clinical development, regulatory workflows, manufacturing operations and commercial infrastructure. We built this market map to make sense of where that’s happening, who is building in each layer and what we think becomes defensible over time.

Key Takeaways

- Drug development is not just a science problem. It’s an operating model problem built on fragmented, people-dependent workflows that AI is now beginning to absorb.

- AI is entering all five layers of the drug development lifecycle: research, drug discovery, clinical trials, regulatory and quality, and commercial.

- The biggest opportunity is not just model performance, but also business model substitution, replacing services spend with AI-native software.

- The most defensible AI life sciences companies will own high-context workflows, generate proprietary data through usage, and expand into systems of record.

Research: From Information Retrieval to Strategic Judgment

The research layer is where the shift begins.

Pharma companies spend heavily on competitive intelligence, KOL research, literature reviews, market landscapes and asset diligence. Much of this work is still performed by analyst teams synthesizing fragmented information across papers, trials, patents, conference abstracts, internal documents and commercial databases.

The pain is not a lack of data. In fact, quite the opposite is true. The industry is drowning in huge quantities of unusable data. The challenge is the inability to turn data into a timely strategic decision.

Elicit, for example, enables researchers to search across massive bodies of academic literature and clinical trial data, generating structured research outputs grounded in systematic review methodology. Convoke is building an operating layer for biopharma knowledge work, unifying internal and external data so teams can automate ad hoc research, build agents for multi-step knowledge workflows and generate first drafts of analyses. Perceptic offers an intelligence layer that unifies internal records, publications, clinical history, and competitive data into a single traceable system, where insights compound across teams and every strategic decision carries the full weight of the organization’s prior knowledge. AI applied to research helps answer critical questions upstream of drug discovery, like where to point R&D efforts based on competitive drugs in market, existing saturation of scientific literature and pipeline white space.

What makes this category especially exciting is the shift from retrieval to reasoning. Earlier generations of pharma intelligence tools surfaced data, but left the synthesis to analysts. The new wave of tools is collapsing the gap between raw evidence and conviction on strategic decisions.

Key Shift

The first generation of tools helped users find information. The current generation helps users decide what matters.

The distinction is critical. Pharma R&D failures are often framed as scientific failures, but many are strategic failures rooted in incorrect targets, wrong indications, weak trial designs, poor competitive timing or unclear differentiation.

The winning companies in this category will not be better search bars. They will become the decision layer for what to prioritize and what to kill, changing the capital allocation equation inside pharma.

Drug Discovery: From Screening to Design

Drug discovery has historically been a brute-force exercise. Identify a target, screen large libraries of known molecules, (hope for a hit!) and then optimize through years of wet-lab iteration…all to achieve industry hit rates of 0.1-0.5%! CROs and lab services companies (such as Charles River Labs and IQVIA) built large businesses around this work because experimentation was expensive (wet lab costs of $70k+ per experiment) and physically constrained.

Generative models invert that workflow.

Instead of starting with a library of molecules that already exist, companies can start with a biological objective and design candidates computationally. Chai Discovery, Isomorphic Labs, Converge Bio and Profluent represent different versions of this future, building models that can reason about things like molecule structure, manufacturability and therapeutic potential before a molecule ever enters the lab.

The results are striking, as Chai’s models are already achieving multiple orders of magnitude higher hit rates and compressing time-to-first-hit from months to weeks, earning the company significant multi-year partnerships with top pharmas like Eli Lilly and Pfizer. We believe the bigger opportunity is just coming into view as biopharma’s hundreds of billions in annual wet lab spend increasingly shifts to the computer and AI meaningfully changes the economics of drug discovery. As the space continues to mature, platforms like Chai will become the competitive frontier that determines which pharma companies out-compete, and ultimately, which drugs get made.

Key Shift

But the next bottleneck is already visible.

If models can generate more plausible candidates, the constraint shifts to experimental validation. Biology still needs to be tested. The question becomes how quickly, cheaply and autonomously teams can close the loop between hypothesis, experiment, result and next experiment.

This is where the AI scientist and AI lab workflow layer becomes important. Phylo’s Biomni Lab gives biologists collaborative agents that can search literature, write and execute code, analyze data and coordinate multi-step experimental workflows, all within a single interface designed around how bench scientists actually work. Edison Scientific’s Kosmos acts as an AI scientist that reads literature, generates hypotheses and executes workflows autonomously across the full R&D pipeline. Together, these tools reflect a broader shift. As generative models raise the ceiling on what’s biologically designable, the bottleneck moves from imagination to execution.

The workflow layer is where that gap gets closed.

The most valuable companies in discovery may not be single-model companies. They may be closed-loop systems that combine models, experiments, data generation and workflow automation. The more proprietary experimental feedback they capture, the stronger their compounding advantage becomes.

Clinical Trials: Rebuilding Pharma’s Largest Operational Bottleneck

Clinical development is the longest, most expensive and most failure-prone stage of the drug lifecycle. Nearly 600,000 clinical trials are registered today, yet almost 80% fail to meet their initial targets and timelines.

AI is attacking clinical development from multiple angles.

Clinical trials are still run by armies of people: CRO project managers, site monitors, patient recruiters, coordinators, medical reviewers and compliance teams. CROs do not just provide expertise; they provide operational capacity. Their business model exists because trial workflows have historically been too complex and fragmented for software to manage end-to-end.

AI is starting to attack that labor layer directly.

Dash Bio is rebuilding the bioanalysis CRO model with a tech-first approach, delivering sample analysis results in days rather than months with transparent fixed pricing and guaranteed outcomes. Alleviate Health deploys AI recruiters that pre-qualify and continuously engage trial candidates through conversational AI. Triomics reads across entire oncology patient records to match every patient against every active trial daily, delivering a pre-screened worklist to providers who can surface high fit candidates.

What’s most exciting is the potential to fix clinical development at every layer, tackling the operational drag that makes trials slow and expensive. Medable (a Sapphire portfolio company) is one of the most comprehensive and mature platforms in this space, bringing agentic AI to the full operational machinery of trial management to automate site monitoring, trial master file processes, and investigator review, while enabling studies to be designed and launched 35x faster than traditional methods.

These companies are not simply selling workflow tools into the existing CRO model. The more ambitious version is to replace parts of the CRO work itself.

This difference is important. Software that makes a CRO 10% more efficient is a feature. Software that lets a sponsor run a faster, cheaper, higher-quality trial with less outsourced labor is a company.

For founders, the wedge matters. Trial software has historically been a difficult category because pharma buyers are risk-averse and legacy systems are deeply embedded. The best AI companies will not win by asking customers to rip everything out. They will win by automating a painful workflow, proving operational reliability, and then expanding into the broader trial execution layer.

Regulatory & Quality: The System of Record Becomes the Moat

Regulatory and quality are some of the most defensible categories within AI life sciences.

The reason is simple. Once a system becomes part of the evidentiary record for how a drug, device or batch was developed, switching costs become enormous. In regulated industries, documentation is not administrative overhead. It is proof.

Pharma spends heavily on regulatory consultants, CMC documentation, quality assurance, validation and audit readiness because the consequences of getting this work wrong are severe. A delayed submission can push revenue back by months. A quality failure can trigger warning letters, remediation work, production delays or worse.

AI has a natural role here because the workflows are language-heavy, evidence-heavy and traceability-heavy.

Valk AI is a customizable AI platform for life sciences that aggregates internal company data and external sources (FDA guidelines, PubMed, ClinicalTrials.gov) to automate workflows across the organization, starting with regulatory submissions, clinical trial protocol design, and quality management, but built to extend across any function from R&D to commercial operations. Collate attacks document generation directly, drafting INDs, NDAs, and other regulatory filings from underlying data with full traceability back to every source.

Manufacturing is an equally attractive frontier.

Drug production still relies on paper logs, aging systems, manual investigations and institutional knowledge. Every batch deviation must be documented in an audit-ready format, yet much of the underlying data remains trapped in disconnected systems.

Katalyze deploys AI agents into existing manufacturing systems to analyze batch data in real time, catch process failures early and automatically generate the audit-ready documentation regulators require.

This category is especially compelling because the data gravity is strong. Once a system understands a company’s products, processes, deviations, submissions and regulatory history, it becomes increasingly valuable over time. The product starts as automation. It becomes infrastructure.

Commercial: The Last Mile

Approval is not the finish line.

A therapy still has to reach physicians, pass through payer controls, clear prior authorization, get routed to the right pharmacy and keep the patient supported over time. This last mile has historically required enormous human infrastructure, including field medical teams, agency partners, reimbursement hubs, patient support teams and case managers.

AI changes both the cost structure and the reach of that model.

OpenEvidence is one of the clearest examples of a new distribution channel in healthcare. Physicians are using AI for clinical guidance at the moment of decision-making. For pharma, that is a fundamentally different surface area than a field rep visit, a conference booth, or a static content portal. It is closer to intent-based distribution for medicine.

Solstice Health automates the creation and compliance review of pharma marketing assets that was previously done via agencies, while BranchLab provides the audience targeting and campaign measurement infrastructure for pharma teams to act on actionable, real-time patient and physician data.

On the patient access side, Forus (fka Tandem), Squad Health and Neon Health are tackling patient access workflows such as prior authorizations, benefit verification and pharmacy routing where administrative friction routinely delays patients from receiving already-approved therapies. Courier Health offers a patient CRM that helps case management teams within biopharma directly manage patient adherence and support after access is granted.

This is not just about cutting headcount.

Key Shift

The more interesting opportunity is that AI enables workflows that were previously impossible at scale.

Pharma brands can reach physicians at the moment they are looking for clinical guidance. Patient support teams can personalize engagement based on real-time context. Access workflows can move from reactive follow-up to proactive orchestration. Commercial teams can understand which interventions actually change patient starts and adherence.

The old commercial model was built around human reach. The new model is built around software-mediated intent, personalization, and workflow automation.

Where Value Accrues

Across all five layers, the same pattern repeats.

AI enters through a narrow workflow that is expensive, manual and painful. It proves reliability in a constrained use case. It captures proprietary workflow data. Then it expands into the adjacent system of record or system of work.

That expansion path is what separates venture-scale companies from useful tools.

In life sciences, we believe the most valuable AI companies will likely share a few characteristics:

- They will own high-context workflows, not generic productivity use cases.

- They will create traceable outputs that regulated buyers can trust.

- They will integrate into existing systems before becoming systems of record.

- They will compound through proprietary data generated by real usage.

- They will replace services spend, not merely sell another software seat.

This last point is the most important.

The AI life sciences opportunity is often described as solely a model performance story. Better models will matter, but the larger economic unlock is business model substitution. Services budgets are large, recurring and painful. If AI-native software can absorb work that previously required consultants, CROs, agencies or large internal teams, the buyer ROI is immediate and the company-building opportunity is much larger.

The Drug Development Stack Is Being Rewritten

The drug development stack is not just getting better software. It is being rebuilt around AI-native labor.

The services organizations that have run pharma’s operational backbone for decades were built because software could not do what they did. CROs, regulatory consultants, medical affairs agencies, manufacturing documentation firms and patient support vendors all existed to absorb complexity that software could not handle.

Now software can absorb the complexity.

That does not mean humans disappear from drug development. In a regulated, scientific, patient-facing industry, expert judgment remains essential. But the ratio changes. The amount of work that can be automated, accelerated, audited and continuously improved expands dramatically.

The opportunity is to rebuild the operating system for how drugs are discovered, tested, approved, manufactured, commercialized and delivered to patients.

If you are building at the intersection of AI and life sciences operations, especially where software can replace services spend and become core infrastructure, we would love to hear from you: Cathy, Aditya, Jasmine, Misty.

Sign up for our newsletter